Libertarian economist Veronique de Rugy writes about it in Reason magazine.

Excerpt:

A word of caution for kids heading off to college this year: Your degree may be worth less and cost more than you think. Your job prospects will likely be grim, whether or not you get that sheepskin. Oh, and you’re on the hook for trillions in federal debt racked up by your parents and grandparents.

Washington has willfully ignored the looming crisis of entitlement spending, knowingly consigning young Americans to a future of crushing debt, persistent underemployment, and burdensome regulation. Politicians on both sides of the aisle share the blame.

This summer, Congress made a big bipartisan show of cutting student loan rates to 3.4 percent from an already artificially low 6.8 percent. But even that seemingly helpful gesture will wind up hurting the Americans it claims to help. Federal student aid, whether in the form of grants or loans, is the main factor behind the runaway cost of higher education. Subsidies raise prices, leading to higher subsidies, which raise prices even more. This higher education bubble, like the housing bubble before it, will eventually pop. Meanwhile, large numbers of students will graduate with more debt than they would have in an unsubsidized market.

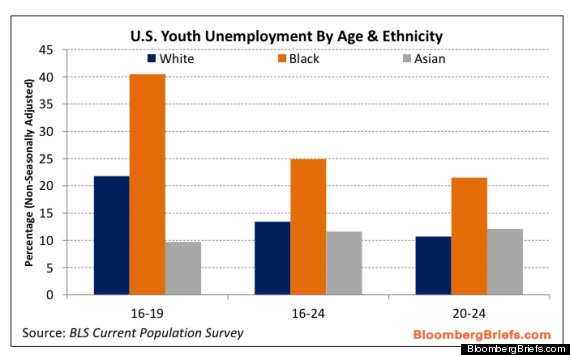

And when those new, debt-laden graduates head out into the labor market with their overpriced diplomas, they may not be able to find a job. According to data provided to me by my Mercatus Center colleague, former Bureau of Labor Statistics (BLS) commissioner Keith Hall, fewer than half of Americans today between the ages of 18 and 25 are employed. For those in that cohort actively on the job market, the unemployment rate is 16 percent, versus 6 percent for job-seekers aged 25 and above.

These young folks are also more likely to be long-term unemployed: While accounting for just 14 percent of the labor force, they make up 19 percent of the long-term unemployed, defined by the BLS as 27 weeks or longer.

The lucky few young’uns with jobs of some kind also suffer from rampant underemployment. In a recent blog post, Diana Carew of the Progressive Policy Institute wrote: “In July 2013, just 36 percent of Americans age 16-24 not enrolled in school worked full-time, 10 percent less than in July 2007.” In other words, of these 17 million young Americans, 5.6 million were working part-time, 3.2 million were unemployed, and 8.4 million were out of the labor force altogether.

I really recommend you read the rest of the article, especially if you aren’t following what Obama’s policies are doing to our economy. Special attention is given to the effects of Obamacare on job creation.

Just as a community service, I want to post for you young people (and your parents) a list of the majors that lead to higher paying jobs:

Top 10 highest-paid college majors

- Petroleum Engineering: $120,000

- Pharmacy Pharmaceutical Sciences and Administration: $105,000

- Mathematics and Computer Science: $98,000

- Aerospace Engineering: $87,000

- Chemical Engineering: $86,000

- Electrical Engineering: $85,000

- Naval Architecture and Marine Engineering: $82,000

- Mechanical Engineering: $80,000

- Metallurgical Engineering: $80,000

- Mining and Mineral Engineering: $80,000

And here are some majors that you should avoid at all costs:

- Counseling Psychology: $29,000

- Early Childhood Education: $36,000

- Theology and Religious Vocations: $38,000

- Human Services and Community Organization: $38,000

- Social Work: $39,000

- Drama and Theater Arts: $40,000

- Studio Arts: $40,000

- Communication Disorders Sciences and Service: $40,000

- Visual and Performing Arts: $40,000

- Health and Medical Preparatory Programs: $40,000

So young people need to be careful what they study in order to get a job that will allow them to pay off all the government debts that their teachers were busy running up. Their teachers taught them that government spending was good, but their teachers aren’t going to be paying for the government spending. They are the beneficiaries of the increased government spending. The pupils are the ones who will have to work to pay for the spending on the social programs enjoyed by their teachers.

It’s very important for young Christians to understand that degrees are getting more expensive, and it’s important to choose a field that is going to produce a return on your investment. Not only do STEM (science, technology, engineering and math) degrees get you a job that pays, but it has other benefits. For example STEM degrees grind out every last bit of impracticality and entitlement-feeling out of you – because in a STEM program, no one cares about your “specialness”. You solve problems or you fail the class. It’s not a situation where you can just repeat what the professor says in order to get good grades, as is often (but not always) the case in the humanities.