This story from Heather MacDonald in the Wall Street Journal is scary.

She writes:

The nation’s two-decades-long crime decline may be over. Gun violence in particular is spiraling upward in cities across America. In Baltimore, the most pressing question every morning is how many people were shot the previous night. Gun violence is up more than 60% compared with this time last year, according to Baltimore police, with 32 shootings over Memorial Day weekend. May has been the most violent month the city has seen in 15 years.

In Milwaukee, homicides were up 180% by May 17 over the same period the previous year. Through April, shootings in St. Louis were up 39%, robberies 43%, and homicides 25%. “Crime is the worst I’ve ever seen it,” said St. Louis Alderman Joe Vacarro at a May 7 City Hall hearing.

Murders in Atlanta were up 32% as of mid-May. Shootings in Chicago had increased 24% and homicides 17%. Shootings and other violent felonies in Los Angeles had spiked by 25%; in New York, murder was up nearly 13%, and gun violence 7%.

Those citywide statistics from law-enforcement officials mask even more startling neighborhood-level increases. Shooting incidents are up 500% in an East Harlem precinct compared with last year; in a South Central Los Angeles police division, shooting victims are up 100%.

By contrast, the first six months of 2014 continued a 20-year pattern of growing public safety. Violent crime in the first half of last year dropped 4.6% nationally and property crime was down 7.5%. Though comparable national figures for the first half of 2015 won’t be available for another year, the January through June 2014 crime decline is unlikely to be repeated.

What could the cause of this be? Well, it’s the backlash against police officers who defend themselves from assault by criminals who attack them:

Since last summer, the airwaves have been dominated by suggestions that the police are the biggest threat facing young black males today. A handful of highly publicized deaths of unarmed black men, often following a resisted arrest—including Eric Garner in Staten Island, N.Y., in July 2014, Michael Brown in Ferguson, Mo., in August 2014 and Freddie Gray in Baltimore last month—have led to riots, violent protests and attacks on the police. Murders of officers jumped 89% in 2014, to 51 from 27.

The state’s attorney general, Eric Schneiderman, wants to create a special state prosecutor dedicated solely to prosecuting cops who use lethal force. New York Gov.Andrew Cuomo would appoint an independent monitor whenever a grand jury fails to indict an officer for homicide and there are “doubts” about the fairness of the proceeding (read: in every instance of a non-indictment); the governor could then turn over the case to a special prosecutor for a second grand jury proceeding.

This incessant drumbeat against the police has resulted in what St. Louis police chiefSam Dotson last November called the “Ferguson effect.” Cops are disengaging from discretionary enforcement activity and the “criminal element is feeling empowered,” Mr. Dotson reported. Arrests in St. Louis city and county by that point had dropped a third since the shooting of Michael Brown in August. Not surprisingly, homicides in the city surged 47% by early November and robberies in the county were up 82%.

Similar “Ferguson effects” are happening across the country as officers scale back on proactive policing under the onslaught of anti-cop rhetoric. Arrests in Baltimore were down 56% in May compared with 2014.

But there’s more – there’s also leniency towards property and drug crime, and criminals are getting the message:

As attorney general, Eric Holder pressed the cause of ending “mass incarceration” on racial grounds; elected officials across the political spectrum have jumped on board. A 2014 California voter initiative has retroactively downgraded a range of property and drug felonies to misdemeanors, including forcible theft of guns, purses and laptops. More than 3,000 felons have already been released from California prisons, according to the Association of Deputy District Attorneys in Los Angeles County. Burglary, larceny and car theft have surged in the county, the association reports.

“There are no real consequences for committing property crimes anymore,” Los Angeles Police Lt. Armando Munoz told Downtown News earlier this month, “and the criminals know this.” The Milwaukee district attorney, John Chisholm, is diverting many property and drug criminals to rehabilitation programs to reduce the number of blacks in Wisconsin prisons; critics see the rise in Milwaukee crime as one result.

Yes, this is what happens with the leftist mainstream media and the Democrats who run big cities like Baltimore, Ferguson, New York, Cleveland, Seattle, etc. get together and decide that they are more opposed to police officers than they are to criminals. If we as a society choose to intimidate and persecute the police for doing their jobs, then crime goes up. What’s my counter to this? Well, it might be time to start thinking about moving out of big cities, especially ones that are run by Democrats. I just don’t see how this is going to get fixed in the near-term, given that Obama rolled back welfare reform, and welfare is what causes women to have children before they get married. Fatherless children are more likely to become criminals. The decline of marriage and family that everyone seems to be celebrating as “tolerance” will just make more delinquent children. So, just when we most need the police (since we insist on attack marriage with welfare, no-fault divorce and same-sex marriage) we are actively working to undermine them.

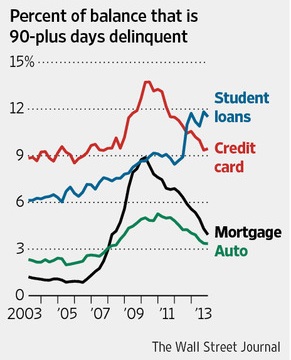

But that’s not all I am seeing that troubles me. I see a lot of support for amnesty, and that means a lot more Democrat voters in the future, especially in states with a high concentration of illegal immigrants. Not only that, but there are problems of underfunded pensions at the state level, and the trillion dollar student loan bubble, and the problem of continued funding of entitlement programs like Social Security. And of course we have the $10 trillion that the Democrats added to the debt, and the problems in so many countries in the Middle East, like Iran, Iraq, Libya, Yemen and Syria. The whole Middle East is on fire, and this is bound to affect us as our defense spending declines.

How to respond to this? I think having earnings and savings is key, and maybe trying to move away from areas that are likely to have high crime, and strains on state and local budgets from illegal immigrants, pension obligations, etc. I really have no answer to the student loan bubble, the entitlements, the debt and the foreign policy threats. What I am doing is focusing on earning money (through work) and saving it by restricting spending on luxury items, e.g. – travel, fun, etc.