I am thinking about moving to a new state in the future, and one of the factors I am considering is underfunded pension liabilities. This basically refers to the ability of a state to pay out pensions to retiring public sector employees going forward. I’m going to tell you everything you need to know to solve this problem in this post.

First, Investors Business Daily explains the problem:

A new report by Hoover Institution Senior Fellow Joshua Rauh shows that, unless action is taken soon, many local governments could face bankruptcy because they can’t meet their pension obligations.

[…]The problem is surprisingly simple: States and cities overestimate returns on their pension fund investments, while systematically underfunding them. The result is a growing deficit that will require massive tax hikes or dramatic and painful cuts in government services and promised pensions to public workers.

Rauh’s study looked at 564 state and local pension systems, representing $4.8 trillion in pension liabilities and $3.6 trillion in assets — for an apparent current deficit of just $1.19 trillion.

So far, so good. But Rauh notes the average expected return on pension assets is about 7.6% — which means a doubling every 9.5 years. He calls that assumption “wildly optimistic,” and says a more realistic assumption would be the Treasury bond rate of 3% or lower — less than half the expected return.

Unless pension managers, politicians and voters do something now, the unfunded liabilities of the national system will continue to grow out of control, reaching $3.4 trillion in just 10 years. States and cities across the country would have to raise taxes massively to keep from becoming insolvent.

Right now, state and local governments set aside about 7.3% of revenues for public pensions. To keep the funding gap from exploding and taking down governments across the nation, pension spending would have to rise to 17.5% of revenues on average — roughly equal to a 240% tax increase.

How did things get so bad? Generations of feckless politicians have refused to face down public employee unions, which have negotiated massively expensive pensions for their members while concealing their true cost. Politicians have gone along with it because, heck, it’s not their money and anyway, the problems will take place long after they’re out of office. That’s where we are now.

States and cities will come under intense pressure to raise taxes on local citizens to pay for this travesty. Instead, they should get rid of the public employee unions that have plundered the public for too long and have made local government inefficient, expensive and dysfunctional. If not, they can expect to face the same economy-crippling effects as Detroit, San Bernardino and a number of other cities have — financial insolvency.

Now, obviously states with kick-ass governors like Scott Walker of Wisconsin are not going to have the same exposure to such problems as incompetent governors like Maggie Hassan of New Hampshire. Scott Walker know how to rein in public sector unions.

Let’s get the numbers to confirm this hypothesis.

Bloomberg has the numbers:

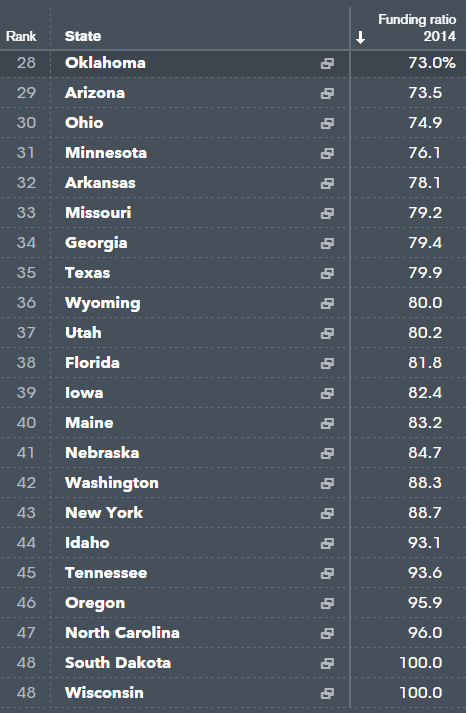

Bloomberg ranked 49 U.S. states based on their pension funding ratios in 2014 under GASB 25. (Delaware is not included because of insufficient data for GASB 25.)

Here are the best states… Wisconsin is 100% funded:

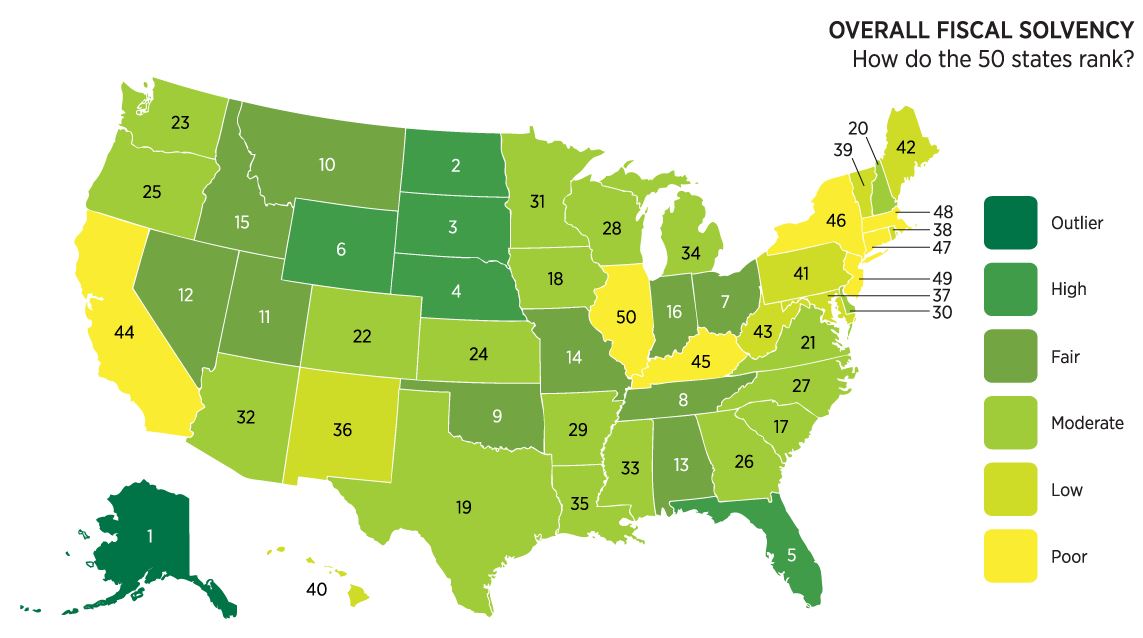

And actually there is a comprehensive analysis of the fiscal solvency of all the states right here from George Mason University.

Here’s the map:

I notice that the deep blue states like California, Massachusetts, Illinois, Connecticut, New Jersey, etc. are just horrible states. No wonder everyone is fleeing them in droves. Socialism doesn’t work. Eventually, the money runs out.

So, if you’re thinking of moving to a new state, look at that. And if you don’t want to move, then vote for governors like Scott Walker who will take on public sector unions – otherwise, you’re headed for a big tax hike in the future, to pay for the big spending liberals of the past.