Young people seem to think that implementing socialism in the United States won’t cost them a thing. The truth is, the rich don’t have enough money to cover all the spending that socialists want to do. It’s going to be young people who are stuck with the bill, and they’ll have to scale their lives down to third world levels to pay for what they voted for.

Here’s a socialist (former bartender) to explain how she would pay for $40 trillion in new spending, over 10 years:

The Daily Wire reports:

TAPPER: “Right. I get that. But the price tag for everything that you laid out in your campaign is $40 trillion over the next 10 years. I understand that Medicare for all would cost more to some wealthier people and to the government and to taxpayers, while also reducing individual health care expenditures. But I am talking about the overall package. You say it’s not pie in the sky but $40 trillion is quite a bit of money. And the taxes that you talked about raising to pay for this, to pay for your agenda, only count for two [trillion dollars]. We’re going by left-leaning analysts.”

OCASIO-CORTEZ: “Right. When you look again at how our health care works, currently we pay — much of these costs go into the private sector. So, what we see, for example, is, you know, a year ago I was working downtown in a restaurant. I went around and I asked how many of you folks have health insurance? Not a single person did. They’re paying — they would have had to pay $200 a month for a payment for insurance that had an $8,000 deductible. What these represent are lower cost overall for these programs. Additionally, what this is, it’s a broader agenda. We do know and acknowledge that there are political realities. They don’t always happen with just a wave of a wand but we can work to make these things happen. In fact, when you look at the economic activity that it spurs — for example, if you look at my generation, millennials, the amount of economic activity that we do not engage in. The fact that we delay purchasing homes, that we don’t participate in the economy as purchasing cars as fully as fully as possible is a cost. It is an externality, if you will, of unprecedented amount of student loan debt.”

TAPPER: “I am assuming I won’t get an answer for the other $38 trillion. We’ll have you back and go over that.”

Some people are going to vote for her just because she’s young, female, and sounds so passionate. But let’s take a look at some numbers so we can understand how feasible her plans are.

First, the rich don’t earn enough money to be able to pay for trillions of dollars in spending.

In 2012, John Stossel wrote this in Forbes:

If the IRS grabbed 100 percent of income over $1 million, the take would be just $616 billion.

In 2011, the Tax Foundation explained that even if you taxed ALL THE DISPOSABLE INCOME from all the people who make $200,000 or more, you would only raise $1.53 trillion dollars:

There’s simply not enough wealth in the community of the rich to erase this country’s problems by waving some magic tax wand.

[…]After everyone making more than $200,000/year has paid taxes, the IRS would need to take every single penny of disposable income they have left. Such an act would raise approximately $1.53 trillion. It may be economically ruinous, but at least this proposal would actually solve the problem.

Socialists want to spend $40 trillion more over 10 years, or about $4 trillion per year. Taking most of what the wealthy earn would make up less than half of that spending.

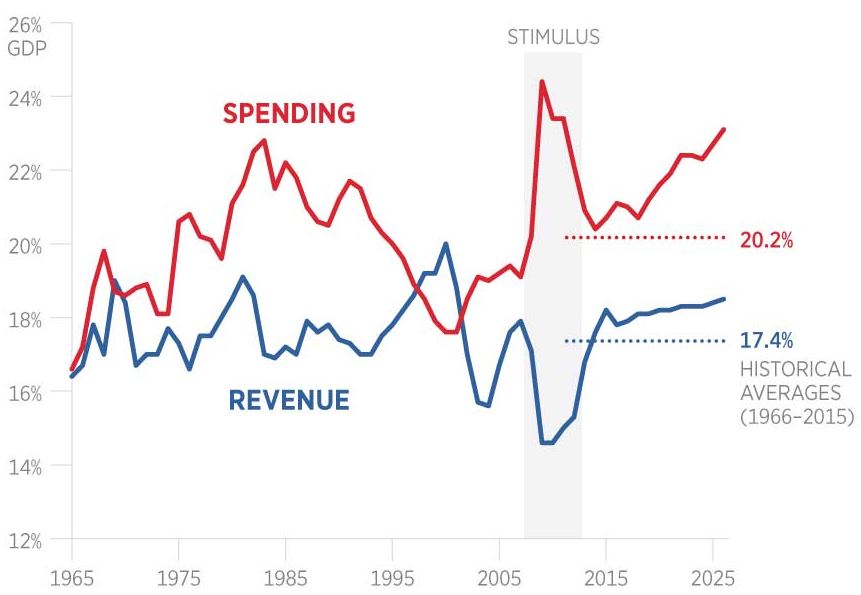

Anyway, we’re not in a position to be doing any spending, because the costs of our existing socialist programs will be increasing going forward.

USA Today explains:

After averaging 35 percent of national income from the mid-1950s through 2008, the national debt has surged to 78 percent today and is projected to reach 100 percent within a decade, and 200 percent by 2050. Even these scary estimates rest on rosy assumptions — no new military or economic crises and creditors willing to accept record-low interest rates from a government heading towards a debt crisis.

Just to be clear, he’s talking about the debt-to-gdp ratio. When ours gets too high, interest on the debt will rise, be ause lenders aren’t sure they’ll be getting their money back. This will put us into a debt death spiral.

More:

The cause of this coming debt deluge is no mystery: Social Security and Medicare are projected to run a staggering $82 trillion cash deficit over the next 30 years. We are adding 74 million retiring baby boomers to a system that provides Medicare recipients with benefits three times as large as their lifetime contributions and pays Social Security benefits typically exceeding lifetime contributions (even accounting for inflation and interest on the contributions).

We can’t afford the spending we’re already committed to right now:

Politicians promise changes to avoid cuts in Social Security and Medicare, but their alternatives are plainly insufficient. Democrats favor tax hikes on the rich, but even doubling the highest two tax brackets to 70 and 74 percent would close just one-fifth of these programs’ shortfalls — and even that assumes people keep working at 90 percent tax rates when including state and payroll taxes. Slashing defense spending to European levels would close just one-seventh of the gap. Single-payer healthcare proposals are projected by even liberal economists to increase the debt. Republicans favor cuts in antipoverty and social spending, but even the unimaginable elimination of all anti-poverty spending would close barely half of the shortfall.

So, who’s going to pay for all this? It will be the people who have to work and pay income taxes for the next 30 years. The very same young Americans who are voting for socialists today. They’re the ones who are going to have to survive on a fraction of what their parents earned.

But there’s more. The truth is that raising taxes on the wealthy will cause enormous damage to job creators. If you look at socialist countries, the unemployment rate among young people is astronomical compared to the USA today. Why? Because these other countries have taxed and regulated businesses so much that they simply don’t have money to hire people, and if they do hire people, they pay them less than what they can earn for the same work in America.

Reuters explains:

Last December, the most recent full figures available, 25 million of the EU’s workforce of 240 million were unemployed and actively looking for jobs, producing an unemployment rate of 11 percent.

An additional 11 million were unemployed but had stopped looking or were not immediately available to start work, and were therefore not classified as unemployed. Adding them to the total would bump the jobless rate up to 15 percent.

Then there were more than 9 million part-time workers who wanted to work more hours but had no opportunity to do so – they were counted as employed but felt underemployed.

And finally there were those who were overqualified for their jobs and might well have been making more money elsewhere if they had found the right match for their skills.

European socialism is a kind of hybrid of socialism and capitalism, so it’s not too bad. In places like Cuba, and Venezuela, you get the real thing. I doubt that most young people really understand what is going on right now on the streets of Cuba and Venezuela. If they did, maybe they wouldn’t be voting for socialism here.