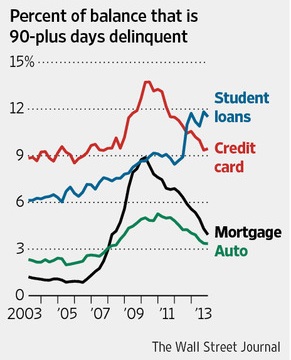

The Wall Street Journal reports on the $1.1 trillion of student loan debt.

Excerpt:

Some Americans caught in the weak job market are lining up for federal student aid, not for education that boosts their employment prospects but for the chance to take out low-cost loans, sometimes with little intention of getting a degree.

[…]A number of factors are behind the growth in student debt. The soft jobs recovery and the emphasis on education have driven people to attain more schooling. But borrowing thousands in low-rate student loans—which cover tuition, textbooks and a vague category known as living expenses, a figure determined by each individual school—also can be easier than getting a bank loan. The government performs no credit checks for most student loans.

College officials and federal watchdogs can’t say exactly how much of the U.S.’s swelling $1.1 trillion in student-loan debt has gone to living expenses. But data and government reports indicate the phenomenon is real. The Education Department’s inspector general warned last month that the rise of online education has led more students to borrow excessively for personal expenses. Its report said that among online programs at eight universities and colleges, non-education expenses such as rent, transportation and “miscellaneous” items made up more than half the costs covered by student aid.

The report also found the schools disbursed an average of $5,285 in loans each to more than 42,000 students who didn’t log any credits at the time. The report pointed to possible factors such as fraud in addition to cases of people enrolling without serious intentions of getting a degree.

Capella Education Co., which runs online schools, examined student costs and debt at institutions public and private in Minnesota and concluded that between a quarter and three-quarters of loans taken out by students were for non-education expenses. At one of Capella’s master’s programs, the typical graduate left with about $30,200 in student debt even though tuition, fees and book costs totaled roughly $18,800. Borrowers are prohibited under federal law, except in rare instances, from discharging student debt through bankruptcy.

The share of student borrowers taking out the maximum amount of loans—$12,500 a year for undergraduates—has risen since the recession. In the 2011-12 academic year, federal Education Department data show, 68% of all undergraduate borrowers hit the annual loan ceiling, up from 60% in 2008.

Research suggests a fair chunk of that is going to non-education expenses. In 2011-12, about a quarter of student borrowers took out loans that exceeded their tuition, after grants, by $2,500, according to research by Mark Kantrowitz, a higher-education analyst and publisher of the education site Edvisors.com.

Some students say they intend to get a degree but must borrow as much as possible because they can’t find decent-paying jobs to cover day-to-day expenses.

Here are some examples of how this is working out:

Tommie Matherne, a 32-year-old married father of five in Billings, Mont., has been going to school since 2010, when he realized the $10 an hour he was making as a mall security guard wasn’t covering his family’s expenses. He uses roughly $2,000 in student loans each year to stock his fridge and catch up on bills. His wife is a stay-at-home mother who also gets loans to take online courses.

“We’ve been taking whatever we can for student loans every year, taking whatever we have left over and using it to stock up the freezer just so we have a couple extra months where we don’t have to worry about food,” says Mr. Matherne, who owes $51,600 in federal loans.

Some students end up going deeper into debt. Early last year, when Denna Merritt lost her long-term unemployment benefits, the 49-year-old Indianapolis woman enrolled part-time at the Art Institute of Pittsburgh’s online program, aiming for a degree in graphic design. She took out $15,000 in federal loans, $2,800 of which went to catch up on unpaid bills, including utilities, health-insurance premiums and cable.

Mr. Selent, of Fort Lauderdale, knows he is getting himself deeper in a hole but prefers that to the alternative of making minimum wage. In his 20s, he earned a bachelor’s degree in communications from a local for-profit school but couldn’t find a job in the field after graduating and began falling behind on his student-loan bills. He is now taking courses for a degree in theater so he can become an actor.

Meanwhile, federal loans allow him to cover any needs that arise during the semester. Says Mr. Selent: “It keeps me from falling apart.”

Wow. Communications and Theatre. Do you think a private bank would have given him money to do a degree in theater? I don’t think so. A private banker might give a loan to someone trying to get a STEM degree, like computer science or nursing, but not for theater. So how did the theater major get the loan, then, if no sane private sector banker would give it to him?

This article from the Heritage Foundation think tank explains how he got the money.

Excerpt:

The Obama Administration’s overreach into the student loan industry has been wide-sweeping. In what The Wall Street Journal deemed “that other government takeover,” a provision buried deep in Obamacare effectively nationalized the student loan industry by ending government subsidies to private lenders and putting the federal government in charge of originating and servicing federally backed student loans.

The Obamacare provision came in addition to the Administration’s decision in 2011—made through executive order—to forgive student loan debt after 20 years. And it comes in addition to the Administration’s gainful employment regulations restricting access to student loans for students attending for-profit institutions.

But the current debate’s origins are in separate legislation passed in 2007 whereby the federal government set interest rates on student loans artificially low, cutting the rates in half temporarily for four years. Now that the interest rates are set to increase, President Obama is pressing Congress to keep rates low.

So the Democrats are repeating the mortgage lending recession they caused in 2008 by again transferring risk away from private banks and onto the backs of the taxpayers. Anybody can get a loan for anything, whether it be basket-weaving or women’s studies or… theater.

It’s just more vote-buying from the Democrat party

The government is giving away these loans to students, no questions asked, in order to buy their votes. These are the students who cheered when Obama promised that they could stay on their parents’ insurance plans until they were 26. The Democrats get the moocher vote, and the students get their loans forgiven in 20 years. Everybody wins – except that the next generation of Americans gets stuck with the bill for this vote buying scheme.