From the Wall Street Journal, a must-read.

Excerpt:

Each month the consultants at Sentier analyze the numbers from the Census Bureau’s Current Population Survey and estimate the trend in median annual household income adjusted for inflation. On Aug. 21, Sentier released “Household Income on the Fourth Anniversary of the Economic Recovery: June 2009 to June 2013.” The finding that grabbed headlines was that real median household income “has fallen by 4.4 percent since the ‘economic recovery’ began in June 2009.” In dollar terms, median household income fell to $52,098 from $54,478, a loss of $2,380.

What was largely overlooked, however, is that those who were most likely to vote for Barack Obama in 2012 were members of demographic groups most likely to have suffered the steepest income declines. Mr. Obama was re-elected with 51% of the vote. Five demographic groups were crucial to his victory: young voters, single women, those with only a high-school diploma or less, blacks and Hispanics. He cleaned up with 60% of the youth vote, 67% of single women, 93% of blacks, 71% of Hispanics, and 64% of those without a high-school diploma, according to exit polls.

According to the Sentier research, households headed by single women, with and without children present, saw their incomes fall by roughly 7%. Those under age 25 experienced an income decline of 9.6%. Black heads of households saw their income tumble by 10.9%, while Hispanic heads-of-households’ income fell 4.5%, slightly more than the national average. The incomes of workers with a high-school diploma or less fell by about 8% (-6.9% for those with less than a high-school diploma and -9.3% for those with only a high-school diploma).

To put that into dollar terms, in the four years between the time the Obama recovery began in June 2009 and June of this year, median black household income fell by just over $4,000, Hispanic households lost $2,000 and female-headed households lost $2,300.

The unemployment numbers show pretty much the same pattern. July’s Bureau of Labor Statistics data (the most recent available) show a national unemployment rate of 7.4%. The highest jobless rates by far are for key components of the Obama voter bloc: blacks (12.6%), Hispanics (9.4%), those with less than a high-school diploma (11%) and teens (23.7%).

This is a stunning reversal of the progress for these groups during the expansions of the 1980s and 1990s, and even through the start of the 2008 recession. Census data reveal that from 1981-2008 the biggest income gains were for black women, 81%; followed by white women, 67%; followed by black men, 31%; and white males at 8%.

[…]Mr. Obama has often contemptuously, and wrongly, branded the quarter-century period of prosperity beginning with the presidency of Ronald Reagan as a “trickle down” era. For many in the groups that Mr. Obama set out to help, a return to the prosperity of that era would be a vast improvement.

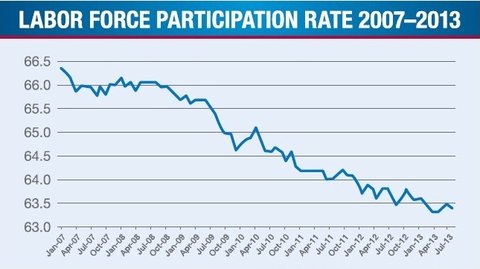

The Census Bureau data on incomes include cash government benefits, such as unemployment insurance, disability payments and the earned-income tax credit (but excludes Medicaid and food stamps). Most of the cash programs have surged in cost during the Obama presidency, yet incomes have still declined for the lowest-income eligible groups. This suggests that wages and salaries from employment have shrunk at an even faster pace than the Census data show. The shrinking paychecks of the past four years are consistent with two unwelcome anomalies of the recovery: a swift decline in labor-force participation to 63.4% from 65.5% during that period and a rise in part-time employment.

What all of this means is that the stimulus-led economic revival that began officially in June 2009—Vice President Joe Biden’s famous “summer of recovery”—has only resulted in lower incomes for at least half of Americans, the very ones who were instrumental in electing Mr. Obama twice.

Guess what? Borrowing trillions from future generations to spend on Democrat-run sham companies like Solyndra doesn’t stimulate the economy. Shocking, I know. And yet that’s what we voted for.

Investors Business Daily explains how the President’s own policies are causing the troubles that his supporters are facing.

Look:

More than 250 employers have cut work hours, jobs or taken other steps to avoid ObamaCare costs, according to a new IBD analysis.

Mind the data have been the refrain from the White House as it downplays anecdotal reports of employers limiting workers to fewer than 30 hours per week.

But the anecdotes are piling high enough that they now constitute a body of data that can help gauge the impact of the Affordable Care Act’s employer mandate.

IBD is introducing ObamaCare Employer Mandate: A List Of Cuts To Work Hours, Jobs — a compilation of employers who have opted to restrict work hours to limit new liability for employee health coverage.

As of Sept. 3, this list has reached 258 — including more than 200 public-sector employers.

Almost all of those employers have cut the hours of part-time workers to below 30 per week — the point at which ObamaCare’s insurance mandate kicks in.

A few have cut payrolls to steer clear of ObamaCare’s 50 full-time-equivalent-worker definition of a large employer subject to employer fines. A few others have reduced staff while contracting with employment services firms to limit their ObamaCare exposure.

The Wall Street Journal explains how health care premiums, which Obama promised to LOWER by $2500, are up $3000.

Excerpt:

Central to ObamaCare are requirements that health insurers (1) accept everyone who applies (guaranteed issue), (2) cannot charge more based on serious medical conditions (modified community rating), and (3) include numerous coverage mandates that force insurance to pay for many often uncovered medical conditions.

[…]We compared the average premiums in states that already have ObamaCare-like provisions in their laws and found that consumers in New Jersey, New York and Vermont already pay well over twice what citizens in many other states pay. Consumers in Maine and Massachusetts aren’t far behind. Those states will likely see a small increase.

By contrast, Arizona, Arkansas, Georgia, Idaho, Iowa, Kentucky, Missouri, Ohio, Oklahoma, Tennessee, Utah, Wyoming and Virginia will likely see the largest increases—somewhere between 65% and 100%. Another 18 states, including Texas and Michigan, could see their rates rise between 35% and 65%.

While ObamaCare won’t take full effect until 2014, health-insurance premiums in the individual market are already rising, and not just because of routine increases in medical costs. Insurers are adjusting premiums now in anticipation of the guaranteed-issue and community-rating mandates starting next year. There are newly imposed mandates, such as the coverage for children up to age 26, and what qualifies as coverage is much more comprehensive and expensive. Consolidation in the hospital system has been accelerated by ObamaCare and its push for Accountable Care Organizations. This means insurers must negotiate in a less competitive hospital market.

Although President Obama repeatedly claimed that health-insurance premiums for a family would be $2,500 lower by the end of his first term, they are actually about $3,000 higher—a spread of about $5,500 per family.

So, every cloud has a silver lining, and the silver lining to this Obama-cloud is that at least the people who voted for socialism are facing the consequences of their own economic illiteracy. I hope they learn. But if they don’t learn now, then they’ll learn when the welfare and entitlements run out. I hope that the people who voted for our American Idol president will take a Thomas Sowell book out of the library and learn something about economics for a change.

UPDATE: From Ian B.: 40,000 Longshoremen (union workers) quit the AFL-CIO union. Socialism hurts employers? It’s all so unexpected! How could reality not match honeyed words and good intentions?