The Heritage Foundation reports on the cases that will determine how far the Democrats can go to undermine religious liberty.

Excerpt:

In less than two weeks, the Supreme Court will hear arguments in cases challenging an Obamacare mandate that is trampling on religious freedom. The Hahn family and the Green family will be at the Court on March 25 asking for respect of their religious liberty and the freedom to continue offering their employees generous health plans.

Let’s meet these families and what they’re fighting for.

A Christian Mennonite family, the Hahns have run Conestoga Wood Specialties near Lancaster, Pennsylvania, for nearly 50 years. A second-generation family business, Conestoga employs almost 1,000 individuals to produce quality wood products.

The Hahns have always run their family business in accordance with their faith, including offering an employee health plan that aligns with their values. Under the mandate, however, Conestoga Wood could face fines of up to $95,000 per day for sticking to their deeply held beliefs and not complying with the mandate.

Speaking of their fight for religious freedom at the Supreme Court, Conestoga president Anthony Hahn explains the magnitude of their case: “It’s not really only for Conestoga; we’re taking a stand for other businesses as well. This is a religious liberty issue that is concerning to us. We feel that the government has gone too far in too many instances.”

And number two:

“We believe that the principles that are taught scripturally are what we should operate our lives by, so that naturally flows over into the business,” explains Steve Green, president of Hobby Lobby, an arts-and-crafts retailer.

Headquartered in Oklahoma City, Hobby Lobby has grown from one 300-square-foot garage to over 500 stores in 41 states employing more than 16,000 individuals.

The Greens’ faith is integral to how they operate their family business. Hobby Lobby storesclose on Sundays and are open only 66 hours a week so that their employees can spend more time with their families. The family’s faith influences not only the way they care for employees but their investment in communities through partnerships with numerous Christian ministries.

Yet under the Obamacare mandate, the government is forcing families like the Greens to violate those beliefs by funding coverage of potentially life-ending drugs and devices or face crippling fines—up to $1.3 million per day in the case of Hobby Lobby. Even if the business is forced to drop employee health care coverage to avoid the mandate, it would still face a fine of $2,000 per employee per year.

There are other victims as well, but these are the two that I am watching. The Obama administration just recently established in the courts that parents have no human right to homeschool their children. Now there will be a fight to see if government can force Christians to violate their consciences in their business operations. We should all be watching and praying about this, and thinking about what we can do to protect our values.

But first, a pretty good introduction to the abortion business:

The abortion business can be very lucrative. Planned Parenthood alone brings in over $150 millionfrom abortion revenues – as much as half of its patient charges. Planned Parenthood destroys over 330,000 unborn children every year, an abortion every 95 seconds, at roughly $468 per abortion. The abortion giant has increased its market share of abortion commerce every year for over 3 decades.

But what has made abortion so profitable has been its constitutionally privileged status and the business model that status has enabled. Unlike virtually any other medical procedure, abortion has been deemed a protected right. This has allowed Planned Parenthood and its industry competitors to resist regulation that other medical services accept as the cost of safely doing business. And by calling on their political friends in high places ( and Planned Parenthood spends millions to keep them in those places) abortion sellers are able to secure political protection from rules that would protect their patients but undercut their bottom line.

Abortion businesses are thus rarely inspected and are often constructed such that women are endangered in an emergency situation. When they are inspected, the inspectors find gross health and safety violations. And as the Gosnell case demonstrates, even their shortcuts on construction can leave women endangered in an emergency situation. Planned Parenthood has also adopted a business plan that has doctors from another state (or country in some cases) fly in, perform dozens of abortions in one day, and then fly back home – leaving the woman with no relationship with the doctor and no opportunity for the doctor to assist in her care in case of complications.

Now the good news – Republicans have been busy passing regulations on this abortion clinics:

In Missouri, Alliance Defending Freedom attorneys Steven Aden and Dale Schowengerdt successfully defended the state’s health and safety regulations of abortion clinics in two challenges in state and federal court. Our friends at 40 Days for Life and others continued to bear witness outside Missouri’s four abortion clinics.

These four were reduced to two over the next few years as providers found their abortion businesses were unprofitable and retired or closed their doors. Then, just last week we received word that, unable to comply with those reasonable health and safety standards, the Columbia, Missouri Planned Parenthood has now lost its license and closed its doors. This leaves only one licensed abortionist operating in Missouri, a Planned Parenthood franchise in St. Louis.

More good news from Alabama, this time:

In Alabama, ADF Allied Attorney Trenton Garmon successfully defended the rights of sidewalk counselors to peacefully pray outside a Birmingham abortion facility. As a result, those sidewalk counselors were there to witness an ambulance transporting an injured woman to a hospital. They reported this to the state health department which investigated and found numerous health and safety violations, resulting in the closure of that abortion facility. This week we learned that the abortionist who owns the facility has given up and placed the building up for sale.

Isn’t that interesting? Rather than comply with the regulations, they choose to shut down. It’s not about providing a service, is it? It’s about the money. And if complying with regulations costs money, then the abortionists just stop providing the service.

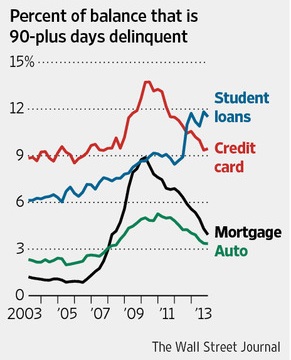

Some Americans caught in the weak job market are lining up for federal student aid, not for education that boosts their employment prospects but for the chance to take out low-cost loans, sometimes with little intention of getting a degree.

[…]A number of factors are behind the growth in student debt. The soft jobs recovery and the emphasis on education have driven people to attain more schooling. But borrowing thousands in low-rate student loans—which cover tuition, textbooks and a vague category known as living expenses, a figure determined by each individual school—also can be easier than getting a bank loan. The government performs no credit checks for most student loans.

College officials and federal watchdogs can’t say exactly how much of the U.S.’s swelling $1.1 trillion in student-loan debt has gone to living expenses. But data and government reports indicate the phenomenon is real. The Education Department’s inspector general warned last month that the rise of online education has led more students to borrow excessively for personal expenses. Its report said that among online programs at eight universities and colleges, non-education expenses such as rent, transportation and “miscellaneous” items made up more than half the costs covered by student aid.

The report also found the schools disbursed an average of $5,285 in loans each to more than 42,000 students who didn’t log any credits at the time. The report pointed to possible factors such as fraud in addition to cases of people enrolling without serious intentions of getting a degree.

Capella Education Co., which runs online schools, examined student costs and debt at institutions public and private in Minnesota and concluded that between a quarter and three-quarters of loans taken out by students were for non-education expenses. At one of Capella’s master’s programs, the typical graduate left with about $30,200 in student debt even though tuition, fees and book costs totaled roughly $18,800. Borrowers are prohibited under federal law, except in rare instances, from discharging student debt through bankruptcy.

The share of student borrowers taking out the maximum amount of loans—$12,500 a year for undergraduates—has risen since the recession. In the 2011-12 academic year, federal Education Department data show, 68% of all undergraduate borrowers hit the annual loan ceiling, up from 60% in 2008.

Research suggests a fair chunk of that is going to non-education expenses. In 2011-12, about a quarter of student borrowers took out loans that exceeded their tuition, after grants, by $2,500, according to research by Mark Kantrowitz, a higher-education analyst and publisher of the education site Edvisors.com.

Some students say they intend to get a degree but must borrow as much as possible because they can’t find decent-paying jobs to cover day-to-day expenses.

Here are some examples of how this is working out:

Tommie Matherne, a 32-year-old married father of five in Billings, Mont., has been going to school since 2010, when he realized the $10 an hour he was making as a mall security guard wasn’t covering his family’s expenses. He uses roughly $2,000 in student loans each year to stock his fridge and catch up on bills.His wife is a stay-at-home mother who also gets loans to take online courses.

“We’ve been taking whatever we can for student loans every year, taking whatever we have left over and using it to stock up the freezer just so we have a couple extra months where we don’t have to worry about food,” says Mr. Matherne, who owes $51,600 in federal loans.

Some students end up going deeper into debt. Early last year, when Denna Merritt lost her long-term unemployment benefits, the 49-year-old Indianapolis woman enrolled part-time at the Art Institute of Pittsburgh’s online program, aiming for a degree in graphic design. She took out $15,000 in federal loans, $2,800 of which went to catch up on unpaid bills, including utilities, health-insurance premiums and cable.

Mr. Selent, of Fort Lauderdale, knows he is getting himself deeper in a hole but prefers that to the alternative of making minimum wage. In his 20s, he earned a bachelor’s degree in communications from a local for-profit school but couldn’t find a job in the field after graduating and began falling behind on his student-loan bills. He is now taking courses for a degree in theater so he can become an actor.

Meanwhile, federal loans allow him to cover any needs that arise during the semester. Says Mr. Selent: “It keeps me from falling apart.”

Wow. Communications and Theatre. Do you think a private bank would have given him money to do a degree in theater? I don’t think so. A private banker might give a loan to someone trying to get a STEM degree, like computer science or nursing, but not for theater. So how did the theater major get the loan, then, if no sane private sector banker would give it to him?

This article from the Heritage Foundation think tank explains how he got the money.

Excerpt:

The Obama Administration’s overreach into the student loan industry has been wide-sweeping. In what The Wall Street Journal deemed “that other government takeover,” a provision buried deep in Obamacare effectively nationalized the student loan industry by ending government subsidies to private lenders and putting the federal government in charge of originating and servicing federally backed student loans.

The Obamacare provision came in addition to the Administration’s decision in 2011—made through executive order—to forgive student loan debt after 20 years. And it comes in addition to the Administration’s gainful employment regulations restricting access to student loans for students attending for-profit institutions.

But the current debate’s origins are in separate legislation passed in 2007 whereby the federal government set interest rates on student loans artificially low, cutting the rates in half temporarily for four years. Now that the interest rates are set to increase, President Obama is pressing Congress to keep rates low.

So the Democrats are repeating the mortgage lending recession they caused in 2008 by again transferring risk away from private banks and onto the backs of the taxpayers. Anybody can get a loan for anything, whether it be basket-weaving or women’s studies or… theater.

It’s just more vote-buying from the Democrat party

The government is giving away these loans to students, no questions asked, in order to buy their votes. These are the students who cheered when Obama promised that they could stay on their parents’ insurance plans until they were 26. The Democrats get the moocher vote, and the students get their loans forgiven in 20 years. Everybody wins – except that the next generation of Americans gets stuck with the bill for this vote buying scheme.