A lot of young people seem to be really excited about socialism, and they want the United States to give it a try. They don’t know where socialism has been tried, and they don’t know what happens with it is tried. It just sounds nice to them.

Well, if you were going to pick one of the most socialist states in the United States, no one would fault you for picking California, where Democrats are running everything, and have been for a long time.

The Washington Free Beacon explains what happened next:

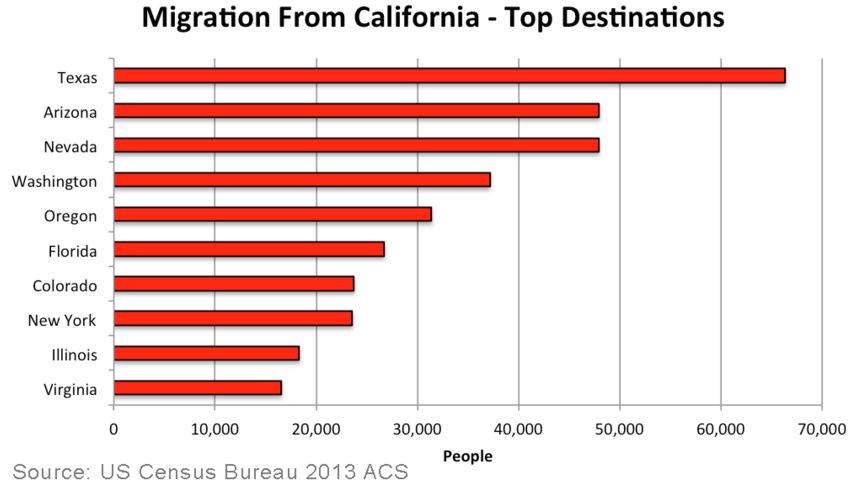

The number of Californians leaving the state and moving to Texas is at its highest level in nearly a decade, according to data from the Internal Revenue Service.

According to IRS migration data, which uses individual income tax returns to record year-to-year address changes, over 250,000 California residents moved out of the state between 2013 and 2014, the latest period for which data was available. The tax returns reported more than $21 billion in adjusted gross income to the IRS.

Of the returns, 33,626 reported address changes from California to Texas, which has been the top destination for individuals leaving California since 2007. Californians who moved to Texas between 2013 and 2014 reported $2.19 billion in adjusted gross income.

[…]“California’s taxes and regulations are crushing businesses, and there are more opportunities in Texas for people to start new companies, get good jobs, and create better lives for their families,” said Nathan Nascimento, the director of state initiatives at Freedom Partners. “When tax and regulatory climates are bad, people will move to better economic environments—this phenomenon isn’t a mystery, it’s how marketplaces work. Not only should other state governments take note of this, but so should the federal government.”

According to Tom Gray of the Manhattan Institute, people may be leaving California for the employment opportunities, tax breaks, or less crowded living arrangements that other states offer.

“States with low unemployment rates, such as Texas, are drawing people from California, whose rate is above the national average,” Gray wrote. “Taxation also appears to be a factor, especially as it contributes to the business climate and, in turn, jobs.”

“Most of the destination states favored by Californians have lower taxes,” Gray wrote. “States that have gained the most at California’s expense are rated as having better business climates. The data suggest that may cost drivers—taxes, regulations, the high price of housing and commercial real estate, costly electricity, union power, and high labor costs—are prompting businesses to locate outside California, thus helping to drive the exodus.”

Just recently, I heard some of my Democrat co-workers laughing to each other about “trickle-down economics”, which is the “ridiculous” idea that if you allow businesses and workers to keep what they earn, then you’ll get more economic growth than if the government takes the money to study the drug use patterns of sex workers in the far East. Actually, we’ve been trying socialism-lite in this country for the past 7 years. How has it worked? Well, Obama has averaged 1.2% GDP growth through his presidency, far below average. And in order to get even that little growth, Obama will double the debt from 10 to 20 trillion in just 8 years.

But what about tax cuts? Do tax cuts create economic growth?

The conservative Heritage Foundation think tank describes the effects of the Bush tax cuts.

Excerpt:

President Bush signed the first wave of tax cuts in 2001, cutting rates and providing tax relief for families by, for example, doubling of the child tax credit to $1,000.

At Congress’ insistence, the tax relief was initially phased in over many years, so the economy continued to lose jobs. In 2003, realizing its error, Congress made the earlier tax relief effective immediately. Congress also lowered tax rates on capital gains and dividends to encourage business investment, which had been lagging.

It was the then that the economy turned around. Within months of enactment, job growth shot up, eventually creating 8.1 million jobs through 2007. Tax revenues also increased after the Bush tax cuts, due to economic growth.

[…]The CBO incorrectly calculated that the post-March 2003 tax cuts would lower 2006 revenues by $75 billion. Revenues for 2006 came in $47 billion above the pre-tax cut baseline.

Here’s what else happened after the 2003 tax cuts lowered the rates on income, capital gains and dividend taxes:

- GDP grew at an annual rate of just 1.7% in the six quarters before the 2003 tax cuts. In the six quarters following the tax cuts, the growth rate was 4.1%.

- The S&P 500 dropped 18% in the six quarters before the 2003 tax cuts but increased by 32% over the next six quarters.

- The economy lost 267,000 jobs in the six quarters before the 2003 tax cuts. In the next six quarters, it added 307,000 jobs, followed by 5 million jobs in the next seven quarters.

The timing of the lower tax rates coincides almost exactly with the stark acceleration in the economy. Nor was this experience unique. The famous Clinton economic boom began when Congress passed legislation cutting spending and cutting the capital gains tax rate.

Regarding the “Clinton economic boom”, that was caused by supply-sider Newt Gingrich passing tax cuts through the House and Senate. Bill Clinton merely signed the bills into law.

Very important to compare times and places where socialism has been tried to times and places where free enterprise and limited government have been tried. We know what works. It may not be what makes us feel smug, but we know what works.