Obama added $10 trillion to the national debt in his 8 years, doubling it from $10 trillion to $20 trillion. That will be placed on the backs of the next generation of younger Americans. But it turns out that they have many other problems as well.

This is from the College Fix.

Excerpt:

In the last two presidential elections, young voters served as a key demographic that helped catapult Barack Obama to the White House. What has he done for millennials in return? According to a new analysis, made them more miserable than ever.

Young America’s Foundation on Wednesday released its annual Youth Misery Index, calculated by adding youth unemployment, student loan debt, and national debt (per capita) numbers.

Today the youth unemployment rate exceeds 16 percent, and the average student in the class of 2015 graduated with a record $35,000 in student loan debt; national debt per capita, “a remarkable burden that will fall squarely on the shoulders of millennials,” is just under $59,000, the foundation reports.

With that, the index has spiked to a record high of 109.9 this year, up from 106.5 last January, and 83.5 in 2009 when President Obama took office, the foundation reports.

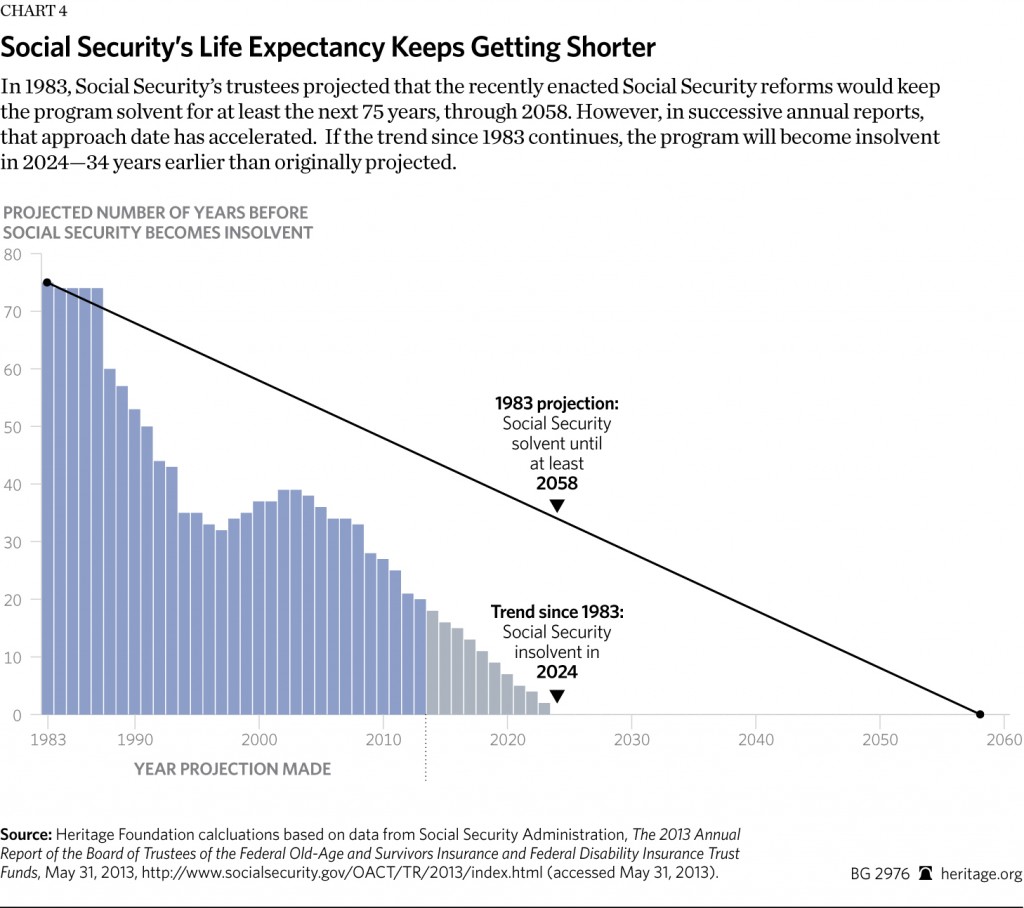

What about entitlement programs?

Business Daily reports on a Social Security problem:

The Social Security Trust Fund just suffered its first annual decline since Congress shored up the retirement program in 1983.

The unexpected $3 billion decline is an indication of the precarious state of Social Security’s finances. Since 2010, the program has been paying out more in benefits than it gets in tax revenue, but the trust fund, which earns about $95 billion a year in interest, had kept growing, though a little less each year.

[…]Under current policies, the CBO says the trust fund will be gone by 2029.

If nothing were done before that point, it would take an across-the-board 29% benefit cut — including on the oldest retirees and the disabled — to bring program costs in line with revenues.

Since we aborted the next generation of workers, we can’t afford to keep paying out benefits at the current rate. There are more people retiring than entering the work force. I hope they start to invest early, but what I am seeing is that they want to take out loans and travel the world for fun and thrills.

Anyway, on to the next problem, trillion dollar deficits. They’re back!

Investors Business Daily explains:

The federal budget deficit is back on the rise — by an expected $105 billion this year — the Congressional Budget Office said Tuesday, the first increase since fiscal 2009. Deficits topping $1 trillion will be back before you know it — three years sooner than expected.

[…]The CBO said the rise was primarily due to the year-end budget deal that extended, and in some cases expanded, corporate and individual tax cuts, as well as busting spending caps. The deficit-to-GDP ratio is expected to grow to 2.9% in fiscal 2016 from 2.5% last year. That would also be the first increase since 2009, with the trend getting worse in the years ahead.

From 2016 to 2025, the CBO expects cumulative deficits of $8.5 trillion — $1.5 trillion more than it predicted in August.

This is the budget deal that establishment Republicans like Paul Ryan supported. Rubio didn’t show up to vote against the Ryan deal. I assume that Rubio was OK with the spending bill passing, and these trillion dollar deficits returning. Cruz showed up to vote against the deal, of course.

And finally, the last problem – Obamacare is making health care more expensive than ever for the middle class.

Investors Business Daily again:

People making just $36,000 a year can easily end up spending 22% of it on health costs, even if they are enrolled in a subsidized ObamaCare insurance plan, according to a report from the Robert Wood Johnson Foundation and the Urban Institute.

[…]Individuals earning between 300% and 400% of the poverty level — which works out to roughly between $35,000 and $47,000 — will pay close to a median of 10% of their income on insurance premiums. (This group is eligible for ObamaCare insurance subsidies but at far lower levels than poorer people.)

And because ObamaCare plans typically come with high deductibles and copays, they’ll spend another 5% on out-of-pocket costs. For a worker making $36,000, the combined costs add up to $5,220.

The report found, however, that these costs could easily double. One in 10 people in this income group will end up devoting 22% of their incomes to insurance and out-of-pocket costs.

Even those in the lowest income group could get hit with big bills. One in 10 of those who make less than 200% of the poverty level will face health costs that eat up 18.5% of their income.

Obama likes to paint a rosy picture of the economy in his state of the union, but the real truth is not so rosy. Young people shouldn’t have voted for him, they are not going to live as prosperously as their elders did under Reagan and George W. Bush.