Of course not, and the voting in Democrats that they seem to like to do is making it worse.

Here’s an article from the Daily Signal to tell about it.

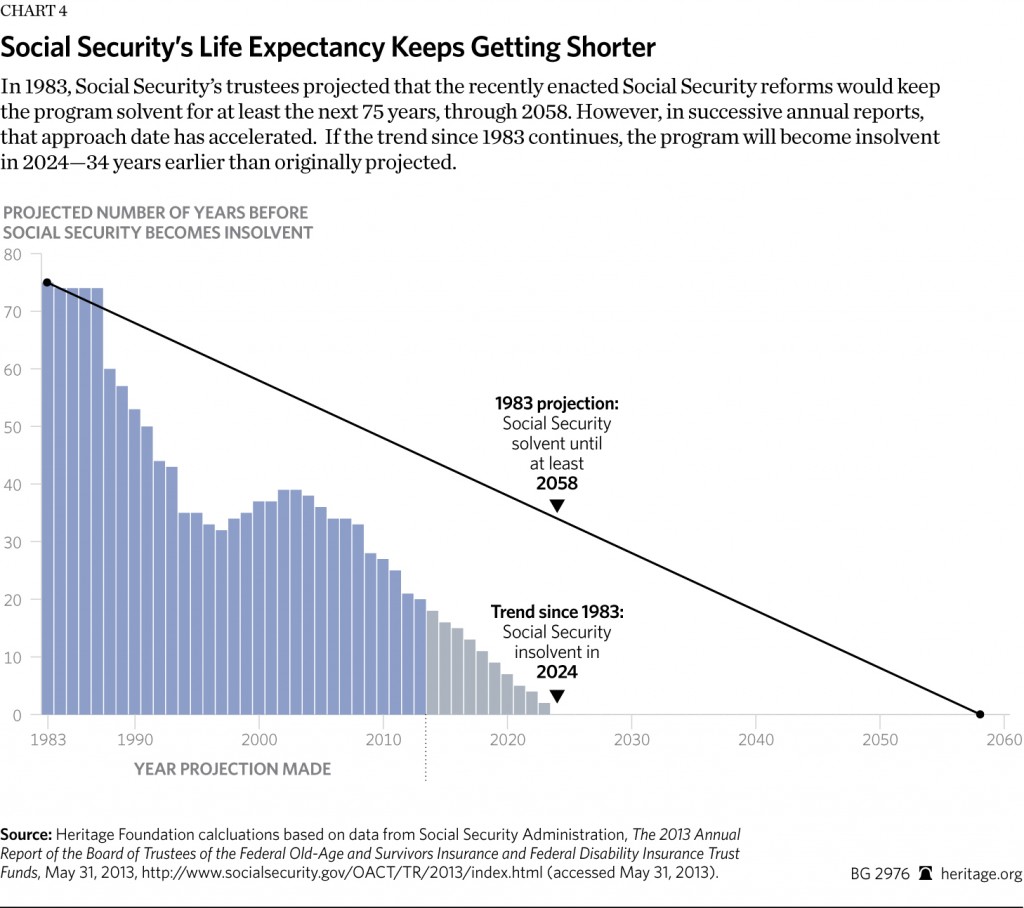

Chart first:

And now the story:

Social Security’s trustees projected in 1983 that the recently enacted Social Security reforms would keep the program active for at least the next 75 years, through 2058. However, according to research by Rachel Greszler, a senior policy analyst, and James M. Roberts, research fellow for economic freedom and growth at The Heritage Foundation, that approach date has accelerated.

“If the trend since 1983 continues, the program will become insolvent in 2024—34 years earlier than originally projected,” Roberts writes.

Now you might think that the way Democrats appeal to younger voters, that they are taking care of this problem for them.

Well, here’s an article from Investors Business Daily.

Excerpt:

The White House recently conceded that President Obama’s executive order effectively legalizing an estimated 5 million undocumented immigrants means that newly legalized workers will contribute to Social Security and Medicare and be eligible for benefits.

Does the president have any idea how much money his action could cost the country — i.e., taxpayers?

[…]The Social Security and Medicare Trust Fund trustees estimate the two program’s combined long-term unfunded liabilities — the estimated amount the government will have to pay in benefits above what it expects to receive — at about $49 trillion. Obama’s amnesty action greatly exacerbates the problem, because retirees get back far more than they pay in.

[…]Because the U.S. pays hundreds of thousands of dollars in retirement benefits, on average, for each new retiree, whether part of Obama’s amnesty program or not, the president has just vastly worsened the long-term financial condition of the country’s two primary retirement safety nets.

But Obama’s newly legalized workers will impose even heavier losses than Steuerle’s examples.

Most workers pay into the programs for their working careers, between 40 and 50 years. But millions of Obama’s newly legalized are working-age adults with children, so many could be in their 40s or older.

Thus they could pay FICA taxes for the next, say, 15 or 20 years — less than half the average American worker — and be eligible for the full array of Social Security and Medicare benefits.

In addition, most will be lower-income workers. The U.S. Bureau of Labor Statistics estimates that foreign-born, full-time workers earn about 80% of native-born Americans ($33,500 vs. $41,900).

Social Security is a social insurance program and is structured to provide disproportionately more benefits for lower-income workers. Medicare pays the same regardless of how much a worker pays in.

To be sure, these new workers’ entry will likely help the trust funds initially, because most will be paying in rather than taking out.

Under current rules, workers must pay FICA taxes for 40 quarters (10 years total) before being fully eligible for the programs. But within a few decades the oldest will start retiring.

Given the demographic unknowns, estimating the amnesty’s financial cost to our retirement programs — and so to U.S. taxpayers — can only be approximate.

But using a basic simulation model, we believe the government will receive about $500 billion in payroll tax revenue (including Part B and drug premiums), and expect it to pay out some $2 trillion in benefits over several decades.

Yeah, so they are actually making it worse. But hey, at least we have redefined marriage, right?

As if that were not enough, there’s this lovely story from CNS News.

Excerpt:

The Daily Treasury Statement that was released Wednesday afternoon as Americans were preparing to celebrate Thanksgiving revealed that the U.S. Treasury has been forced to issue $1,040,965,000,000 in new debt since fiscal 2015 started just eight weeks ago in order to raise the money to pay off Treasury securities that were maturing and to cover new deficit spending by the government.

The only way the Treasury could handle the $942,103,000,000 in old debt that matured during the period plus finance the new deficit spending the government engaged in was to roll over the old debt into new debt and issue enough additional new debt to cover the new deficit spending.

This mode of financing the federal government resembles what the Securities and Exchange Commission calls a Ponzi scheme. “A Ponzi scheme,” says the Securities and Exchange Commission, “is an investment fraud that involves the payment of purported returns to existing investors from funds contributed by new investors,” says the Securities and Exchange Commission.

“With little or no legitimate earnings, the schemes require a consistent flow of money from new investors to continue,” explains the SEC. “Ponzi schemes tend to collapse when it becomes difficult to recruit new investors or when a large number of investors ask to cash out.”

Now you might ask yourself – are young people aware of these things? Of course not. What they learn in university is how to escape their repressive religious backgrounds by experimenting with risky, irresponsible sexual behavior. They are not aware of the situation, and when they vote, they vote like they were picking candidates on American Idol. I guess I can understand why young people act stupidly. They are concerned with what the culture tells them to be concerned about, and that’s legal baby-killing, redefining marriage to separate kids from their mom or dad, police shooting people who commit crimes, a nonexistent gender pay gap and global warming. What is appalling to me is when their parents vote Democrat… which is basically voting to have a higher standard of living for themselves, then passing the bill onto to their kids. It’s especially amazing when married women do this to their own kids. What are they thinking?