First, the problem, using this article from New Zealand. It is authored by a self-made millionaire to young people.

Excerpt:

A young property tycoon has hit out at Generation Y claiming they need to stop travelling and spending money on overpriced food if they want to save for their first home.

Tim Gurner, 35, is worth nearly half a billion dollars since buying his first investment property at the age of 19.

The Melbourne millionaire believes it’s time his generation change their spending and lifestyle habits.

“When I was trying to buy my first home, I wasn’t buying smashed avocado for $19 and four coffees at $4 each,” he told Channel Nine’s 60 Minutes program.

“We’re at a point now where the expectations of younger people are very, very high. They want to eat out every day, they want travel to Europe every year.

“This generation is watching the Kardashians and thinking that’s normal – thinking owning a Bentley is normal.”

And how did the millennials respond? With immature, ignorant rebellion:

Gurner’s comments have been met with a backlash on social media will many criticising how he started out in the property – with a loan from his grandfather.

One social media comment read: “Maybe the new home buyers would stand more of a chance if they were given 34K by their grandad… that’s a fair few smashed avos.’

Another added: ‘Nice if you can get it,’ while one commented: ‘Much like Trump’s dad gave him a “small loan of $1Mil.’

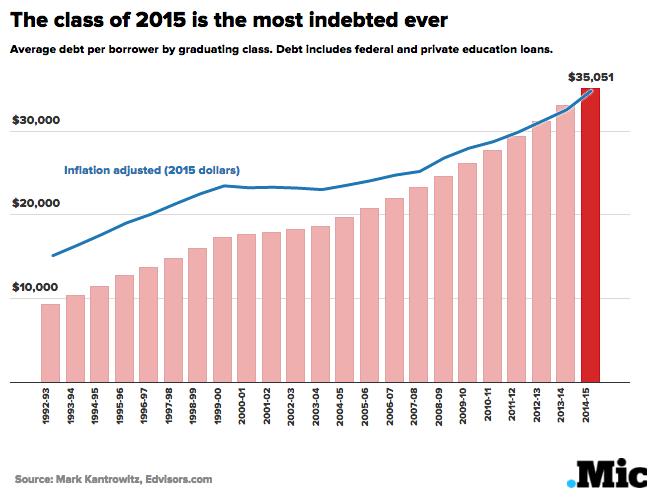

Of course, the average college graduate HAS actually borrowed that much money (see graphic above), but they just preferred to blow it all on alcohol, birth control and a degree in English literature.

Speaking of a degree in English literature…

This woman complained to her boss because she wasn’t making enough money. She graduated with a non-STEM degree (English literature), and lives in one of the most expensive cities in America. (The cities that are all run by leftist Democrats who love to spend money on public works and welfare). She didn’t even have roommates to split the rent!

I see this in so many young people – complete disregard for the future in order to have fun, thrills and frivolous travel right now. And all their same-age friends support their decision-making. Young people don’t listen to grown-ups who have experience and real achievements. They listen to their friends. I know one woman who literally flew off to be a missionary in Europe for two years, on the advice of two Christian students, neither of which had ever worked a full-time job or saved money. They were proudly living off their parent’s incomes into their late-20s, and she looked to them for advice on education, career and finances.

Low-income earners can still save money

You don’t have to have a great job to make choices that lead to growing your wealth.

Here is an article from Business Insider about how to build wealth on a minimum wage salary.

Excerpt:

Here are the key expenses that someone on minimum wage can consider cutting, to make an immediate impact:

- Moving to a more affordable city can cut living expenses considerably. It’s hard to accumulate wealth in Manhattan or San Francisco, but is much more likely in Buffalo or Memphis.

- Eliminate commuting. Cars are expensive, and it is possible to get a place close enough to work to bike.

- Cut some wires, particularly cable. After all, it’s 2017 – just go with internet and Netflix.

- Don’t eat out, unless it’s absolutely necessary.

- Skip most purchases of new clothes. Instead, make thrift stores your new best friend, and don’t be afraid to mend holes in clothing.

- Cut expensive activities, and rediscover that the best things in life are free. Playing many sports can be free (or cheap), and public libraries are free (or cheap).

Once that’s done – it’s all about investing in yourself.

The Obama administration set interest rates low for the last eight years, encouraging people to borrow more and more money – money that they could not pay back. Thankfully, the private sector has ways of encouraging people to save money.

This article is from the far-left The Atlantic.

Excerpt:

Late last summer, Dawn Paquin started keeping her money on a prepaid debit card from Walmart instead of in a traditional checking account. The wages from her factory job—she works from 9 p.m. to 5 a.m., inspecting blades on industrial bread-slicing machines—now go directly onto the Visa-branded card, which she can use like a regular debit card, though unlike most debit cards, it is not linked to a checking or savings account.

[…]The card is more convenient, Paquin said, and she doesn’t have to worry about monthly statements; she tracks her money, and pays all her bills, with the card’s associated phone app.

[…]In a 2015 Federal Reserve Board survey, 46 percent of respondents reported that they would have trouble coming up with $400 in an emergency; living paycheck to paycheck is now a commonplace middle-class experience. So while Paquin noticed that her Walmart MoneyCard app asked her from time to time whether she wanted to “stash” some money, she didn’t bother to figure out what that actually meant, let alone respond.

Then, late last year, she got an email saying that a “prize savings” feature had been added to her card. If she kept some of her balance in a virtual “vault,” meaning that it would not show up in her available funds, she would be eligible to win a cash prize in a monthly drawing—up to $1,000. Every dollar in the MoneyCard Vault would equal an entry in that month’s drawing. This caught her interest. A prize would go a long way toward her being able to buy a car. It also made her focus on what all those “stash” requests were about. “Oh, cool, this can work as a savings account, too,” she remembers realizing. So when she got paid, she started setting aside “10 bucks, 20 bucks, whatever I could.”’

[…]The program was launched to a limited number of MoneyCard holders in August, offering 500 prizes a month—one for $1,000, the rest $25 each. In December, the company reported that the number of Vault users had grown more than 130 percent, to more than 100,000, and that the average savings had grown from $413 to $572, a 38 percent increase.

Paquin actually did end up winning the $1000 prize for stashing some of her earnings. And she saved most of it, of course. Because she learned from the incentives.