I saw a bunch of pro-marriage friends were tweeting about this article from the St. Louis Federal Reserve which talks about how well married men do financially compared to single men, and using it as a reason to argue that men should get married. The article from the St. Louis Reserve doesn’t have much commentary, but this article from the far-left Washington Post by Brad Wilcox has a lot to say.

Excerpt:

Marriage has a transformative effect on adult behavior, emotional health, and financial well-being—particularly for men.

[…]Men who get married work harder and more strategically, and earn more money than their single peers from similar backgrounds. Marriage also transforms men’s social worlds; they spend less time with friends and more time with family; they also go to bars less and to church more.

[…]Our research, featured in a recent report, “For Richer, For Poorer: How Family Structures Economic Success in America,” indicates that men who are married work about 400 hours more per year than their single peers with equivalent backgrounds. They also work more strategically: one Harvard study found that married men were much less likely than their single peers to quit their current job unless they had lined up another job.

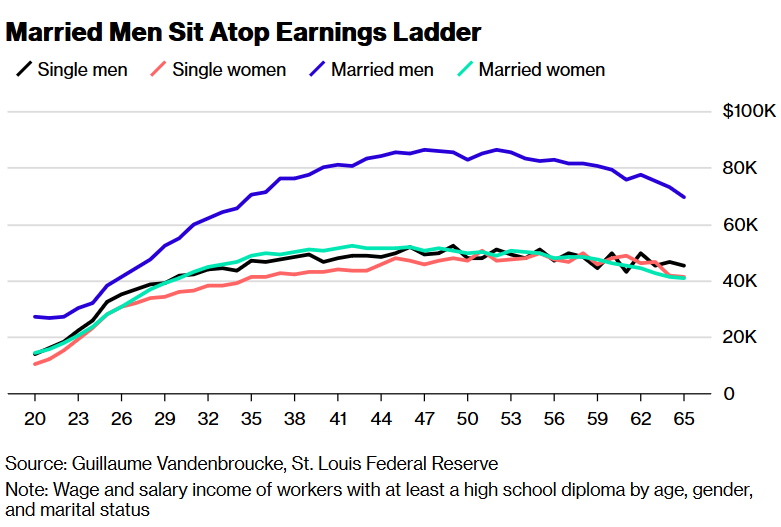

This translates into a substantial marriage premium for men. On average, young married men, aged 28-30, make $15,900 more than their single peers, and married men aged 44-46 make $18,800 more than their single peers.

That’s even after controlling for differences in education, race, ethnicity, regional unemployment, and scores on a test of general knowledge. What’s more: the marriage premium operates for black, Hispanic, and less-educated men in much the same way as it does for men in general.

For instance, men with a high-school degree or less make at least $17,000 more than their single peers.

So, what about these differences between married men and single men? Are men able to earn more if they have a wife to support them and care for their needs? Or is it just that women prefer men who are already able to take care of themselves?

Well, in most cases, it’s the former:

2. Married men are motivated to maximize their income. For many men, this responsibility ethic translates into a different orientation toward work, more hours, and more strategic work choices. Sociologist Elizabeth Gorman finds that married men are more likely to value higher-paying jobs than their single peers.

This is partly why studies find that men increase their work hours after marrying and reduce their hours after divorcing. It’s also why married men are less likely to quit a current job without finding a new job. Indeed, they are also less likely to be fired than their single peers.

3. Married men benefit from the advice and encouragement of their wives. Although there is less research on this, we suspect that men also work harder and more strategically because they are encouraged to do so by their wives, who have an obvious interest in their success. One study appears to buttress this point, finding that men with better-educated wives earn more, even after controlling for their own education.

4. Employers like married men with children. There is evidence that employers prefer and promote men who are married with children, especially compared to their childless male peers and to mothers. Married men are often seen as more responsible and dedicated workers and are rewarded with more opportunities by employers. While illegal bias and long-held stereotypes appear to play a role in this historic preference, it nonetheless helps explain why married family men get paid more.

Now what’s the purpose of me writing this? Well, I’m actually NOT writing this to pressure men to get married. Why not? Because although marriage was a pretty good deal 100 years ago, it’s not as good of a deal under the current laws and policies, e.g. – no-fault divorce, the threats of false accusations, the Sexual Revolution, etc. The institutions of society are not doing as good of a job to prepare women for wife and mother roles as they used to do. Men have a much harder time finding someone who is prepared for marriage today. Men have to choose women more carefully.

But I am writing this to women who are being told by the culture to delay marriage, and especially to delay marriage to use your youth and beauty to “have fun” with boys who won’t commit to marriage. If a woman loves a marriage-focused man and really wants to take care of him and support him, then early marriage is one of the very best ways to really help him during the years (22-45) when it really makes a difference. Marrying a man who wants marriage when you’re still young means that he will have many, many measurable benefits. It’s hard to attract a man who is already rich, because so many women are competing for him. It’s much easier to marry a young man and build him up into a rich man, by supporting him.

Men know that a woman’s support has value. It’s important for women to marry when the marriage has the potential to do the most good for a man in areas like health, career, finances and children. Men typically don’t want to marry women who are older, because those women tend to have more sexual experience. They get used to giving a man sex in order to get him to do what she wants. They get used to breaking up instead of making things work. Once a woman gets used to doing this, it becomes much harder to trust a good man to lead, and to give a man respect as a leader.

So, what I would like to see is women understand that part of loving a man is committing to him early, and staying with him to build him up. Instead of trying to wasting your youth on hot bad boys, why not build up a good man into the fit, wealthy husband you want? It seems to me that building up a man into what you want is a lot easier than wasting your youth on bad boys, then trying to attract a good man when your attractive years are already behind you.