First, let’s recall what the socialist leader Tsipras said after he was elected to save nearly bankrupt Greece.

Look how the radically leftist UK Guardian gushed when Tsipras took office:

In a dramatic start to his tenure in office, Greece’s new prime minister, Alexis Tsipras, has begun unpicking the deeply unpopular austerity policies underpinning the debt-stricken country’s bailout programme.

[…]“We won’t get into a mutually destructive clash, but we will not continue a policy of subjection,” said Tsipras, who at 40 is Greece’s youngest postwar leader.

[…]Earlier, the energy minister, Panagiotis Lafazanis, called a halt to the privatisation programme that the EU and IMF have demanded in exchange for the €240bn in aid keeping Greece afloat. Plans to sell off the country’s dominant power corporation, PPC, were to be frozen with immediate effect. “We will immediately stop any privatisation of PPC,” said the politician, who heads Syriza’s militant Left Platform. A proposed scheme to privatise the port of Pireaus, the country’s largest docks, were also put on hold.

Yes, only nasty conservatives like me think that private industry is cheaper, more efficient and less corrupt than big government for handling big projects.

More:

After that, ministers announced more measures: the scrapping of fees for prescriptions and hospital visits, the restoration of collective work agreements, the rehiring of workers laid off in the public sector, the granting of citizenship to migrant children born and raised in Greece. On his first day in office – barely 48 hours after storming to power – Tsipras got to work. The biting austerity his Syriza party had fought so long to annul now belonged to the past, and this was the beginning not of a new chapter but a book for the country long on the frontline of the euro crisis.

“A new era has begun, a government of national salvation has arrived,” he declared as cameras rolled and the cabinet session began. “We will continue with our plan. We don’t have the right to disappoint our voters.”

If Athens’s troika of creditors at the EU, ECB and IMF were in any doubt that Syriza meant business it was crushingly dispelled on Wednesday . With lightning speed, Europe’s first hard-left government moved to dismantle the punishing policies Athens has been forced to enact in return for emergency aid.

Measures that had pushed Greeks on to the streets – and pushed the country into its worst slump on record – were consigned to the dustbin of history, just as the leftists had promised.

Yes, everything is going to be sunshine and roses, because a 40-year-old know-nothing with no experience says it will be. Economics? That dismal science belongs in the dustbin of history. We can unilaterally reverse the policies our creditors demanded, and then they will of course keep lending us money anyway.

Another leftist UK Guardian article has more happy rhetoric and socialist policies:

Dismantling the EU-IMF mandated measures that had plunged Greece into poverty and despair would, declared Panos Skourletis, the labour minister, be his single greatest priority.

“The reinstatement of the minimum wage to €751 (£560) [a month] will be among the government’s first bills,” Skourletis announced on Antenna TV.

Under international stewardship, Athens had been forced to pare back the minimum wage to under €500, ostensibly to increase competitiveness and make the labour market more attractive. Skourletis, formerly Syriza’s hard-nosed spokesman, said plans were similarly under way to bring back collective work agreements – a major demand of unions – and to annul the enforced mobilisation of workers protesting against cuts.

Everything is awesome! Well, those two articles were from January 2015. Let’s see what’s happening now.

This is from UK Telegraph:

Greece’s “war cabinet” has resolved to defy the European creditor powers after a nine-hour meeting on Sunday, ensuring a crescendo of brinkmanship as the increasingly bitter fight comes to a head this month.

Premier Alexis Tsipras and the leading figures of his Syriza movement agreed to defend their “red lines” on pensions and collective bargaining and prepare for battle whatever the consequences, deeming the olive-branch policy of recent weeks to have reached a dead end.

“We have agreed on a tougher strategy to stop making compromises. We were unified and we have a spring our step once again,” said one participant.

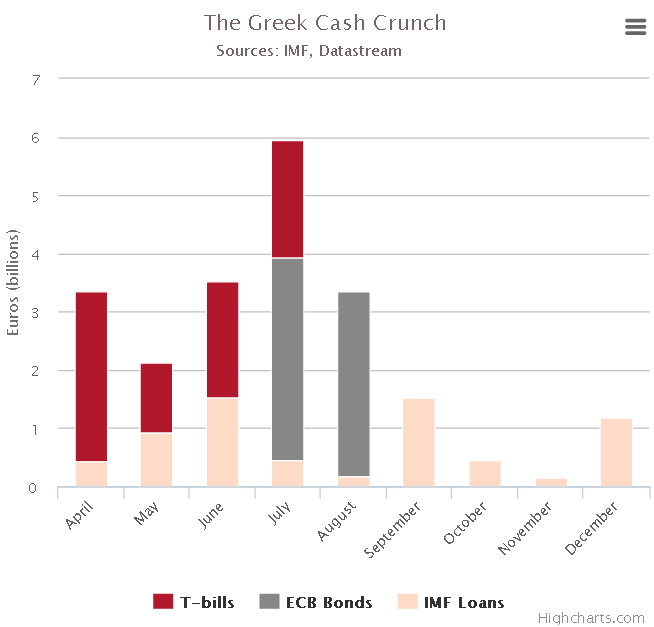

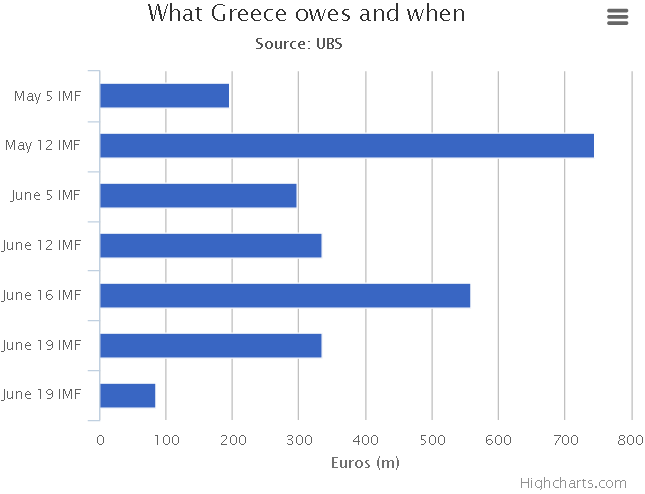

The Syriza government knows that this an extremely high-risk strategy. The Greek treasury is already empty and emergency funds seized from local authorities and state entities will soon run out.

Greece’s mayors warned over the weekend that they would not release any more funds to the central government. The Greek finance ministry must pay the International Monetary Fund €750m (£544m) on Tuesday, the first of an escalating set of deadlines running into August.

“We have enough money to pay the IMF this week but not enough to get through to the end of the month. We all know that,” said one minister, speaking to The Telegraph immediately after the emotional conclave.

If there’s one thing that makes me feel better about all the crap that is happening in this world, it’s the wonderful truth that eventually, bad economics meets with reality. You can imagine anything you want today that makes you feel good, and imagine that it will all be paid for somehow in the future. I really like it when people who don’t have any money make these elaborate future plans and then bet their futures on it. Because when reality comes, we all find out that there is justice in the world after all. There is no path to prosperity that involves doing whatever you want and being happy all the time – that is a myth that children have about life. Anyway, pass me the popcorn and let’s see how the Peter Pan plans of these inexperienced children work out. We won’t have to wait long. Mmm, this popcorn tastes schadenfreudelicious.