Let me start with the facts from Breitbart News, and then I’ll comment on the part in bold.

Excerpt:

Study after study shows that Americans are not saving for retirement like they should, and a new survey finds that nearly one third of people who have some sort of savings plan have amassed less than $1,000 for retirement.

The survey titled “Preparing for Retirement in America,” by Employee Benefit Research Institute (EBRI) and Greenwald and Associates, finds that only 65 percent of workers have any savings for retirement, a number that fell below the 75 percent figure from 2009.

But 28 percent of workers report that they have saved less than $1,000 for retirement, and almost 6 in 10 Americans say that their financial planning needs improvement.

Additionally, 34 percent say they have made no effort at all to saving anything or make a retirement plan. Still, most say that they intend to start saving at some point.

But intentions may not be enough. “Intending one thing and doing another is human, but it’s an impulse we should all fight hard to resist,” Rebekah Barsch, vice president of planning and sales at Northwestern Mutual, said in a press statement. “Intentions only get us so far. And when the stakes are high, it’s taking action that’s critical.”

Many say that the average person needs to save one million dollars for retirement, but a recent piece by David Marotta, president of Marotta Wealth Management in Charlottesville, VA, noted that a 20-year-old in 2015 may have to amass up to $7 million to retire comfortably.

“Someone retiring now in 2014 with $1 million at age 65 can safely withdraw $43,600 a year,” Marotta wrote last May. “However, [because of inflation], today’s 20-year-olds will need over $7 million to have that same lifestyle when they retire. In 1970, they would only have needed $166,000 in retirement to have a similar purchasing power for the rest of their life.”

Many Americans save for retirement using the 401K plans provided through their employer, but according to the federal government, around 50 million Americans don’t have the ability to enroll in such a savings plan.

Here’s a helpful article from CNBC that answers the question “how much do I need to retire?”.

It says:

You can’t feel secure in retirement if you don’t have a good idea of how much money you’ll need.

But if you believe a new Legg Mason survey, you may have to save far more than you think. Investors surveyed by the global investment management firm said they will require an average of $2.5 million in retirement to enjoy the quality of life they have today.

That’s about $2.2 million more than the average balance of $385,000 those investors actually had in 401(k)s and similar retirement plans, which might help explain why only 40 percent of the 458 investors surveyed said they are “very confident” in their ability to “retire at the age I want to.” (And the investors surveyed have set more aside than the average retirement saver. At Fidelity, the nation’s largest retirement plan provider, the average 401(k) balance was $91,300 at the end of 2014.)

[…]Fidelity estimates most investors require about eight times their ending salary to increase the chances that their savings will last during a 25-year retirement. But every retirement is different. People also tend to spend lavishly in their first years of retirement before their spending declines in later years.

Health care is the wild card in retirement planning, especially as Americans live longer. Fidelity projects a 65-year-old couple retiring will need an average of $220,000 to cover medical expenses in retirement.

So, according to Fidelity’s rule, if you are single and making $50K after taxes, then you need $400,000 to retire at age 65. You’ll need more the earlier you retire. That seems about right to me. The important thing to do when planning for the future is not to imagine a higher income than you have right now, though. Imagining that things will be better than they are right now is a terrible mistake. You can’t make the world change just by imagining things that make you feel good, or by looking at cherry-picked examples from people you know who got lucky.

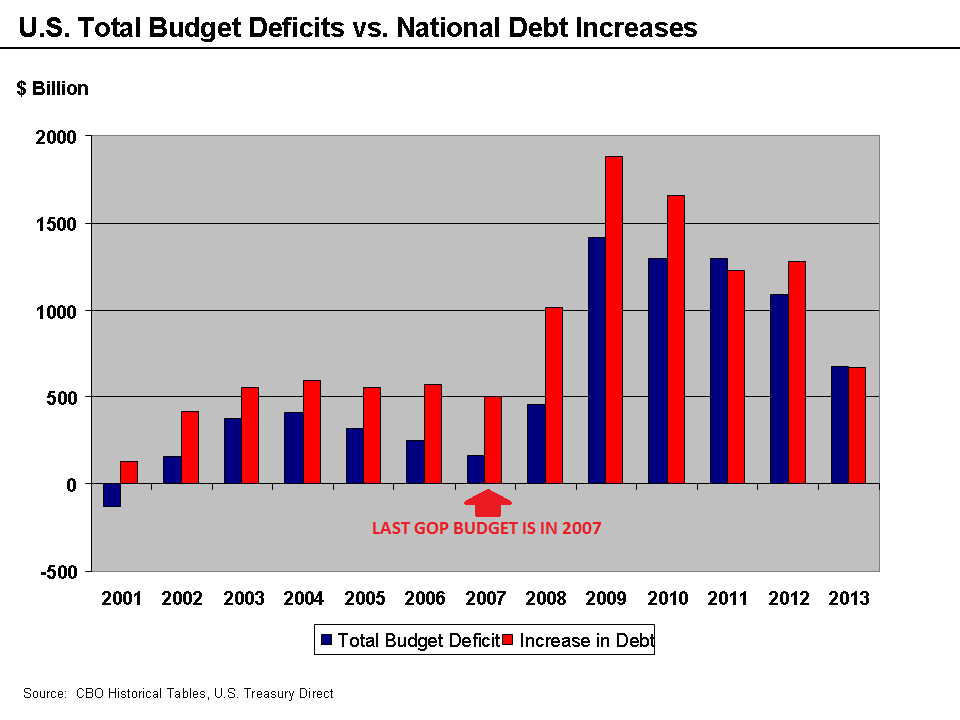

The trouble with young people today is that they think that things tomorrow will be the same as they were yesterday. They don’t see the future implications of running our national debt up to $18.5 trillion dollars. They think entitlement programs will be solvent when they are ready to retire. They aren’t aware of what’s going on in the economies of other countries that we trade with. They aren’t aware of what’s going on in Greece, and how that will affect the European Union. They aren’t aware of the demographic crisis in Europe, and especially in Japan. They aren’t thinking about the implications for future wars as America withdraws from the world stage. And so on. And since they are not aware, they are delaying making a plan to save, so they can have more fun now. Their retirement plan is all future sunshine and rainbows, but no actions are being taken right now.

If I could give young people one piece of advice, it’s this. It’s much easier to shift your life out of a position of financial security to something lighter but more meaningful in the second half of your life. It’s harder to work back to earning and saving if you have squandered your early life on fun, thrills, travel, non-STEM degrees, etc. If you’re 30 years old and don’t have any savings, you are in serious, serious trouble. You need to get focused on a regular career as soon as possible, and start saving. Get those debts paid off now. Still think that your rosy picture of the future will obtain? Usually, you can tell how good you are at strategic forecasting by looking at your past decisions. Have you been wise before, or have you chosen poorly? If you’ve chosen poorly, then it’s a good idea to defer to people who haven’t made the same mistakes. If you’re an optimistic person who is always being surprised and disappointed, that’s a good sign you need to start saving now.