Well, the law was supposed to take until now to come into full effect. Now that we are getting the full Obamacare, what are we seeing?

The Wall Street Journal says not enough of the young Democrats who voted for Obamacare are signing up for it:

This month the Health and Human Services Department dramatically discounted its internal estimate of how many people will join the state insurance exchanges in 2016. There are about 9.1 million enrollees today, and the consensus estimate—by the Congressional Budget Office, the Medicare actuary and independent analysts like Rand Corp.—was that participation would surge to some 20 million. But HHS now expects enrollment to grow to between merely 9.4 million and 11.4 million.

Recruitment for 2015 is roughly 70% of the original projection, but ObamaCare will be running at less than half its goal in 2016. HHS believes some 19 million Americans earn too much for Medicaid but qualify for ObamaCare subsidies and haven’t signed up. Some 8.5 million of that 19 million purchase off-exchange private coverage with their own money, while the other 10.5 million are still uninsured. In other words, for every person who’s allowed to join and has, two people haven’t.

Among this population of the uninsured, HHS reports that half are between the ages of 18 and 34 and nearly two-thirds are in excellent or very good health. The exchanges won’t survive actuarially unless they attract this prime demographic: ObamaCare’s individual mandate penalty and social-justice redistribution are supposed to force these low-cost consumers to buy overpriced policies to cross-subsidize everybody else. No wonder HHS Secretary Sylvia Mathews Burwell said meeting even the downgraded target is “probably pretty challenging.”

The program doesn’t work unless young, poor, healthy people are forced to pay for the health care of rich, older, sickly people.

The radically leftist New York Times reports that out of the 22 health insurance co-ops Obamacare created, nine of them have already closed – leaving customers without coverage.

Excerpt:

The grim announcements keep coming, picking up pace in recent weeks.

About a third, or eight, alternative health insurers created under President Obama’shealth care law to spur competition that might have made coverage less expensive for consumers are shutting down. The three largest are among that number. Only 14 of the so-called cooperatives are still standing, some precariously.

The toll of failed co-op insurers, which were intended to challenge dominant companies that wield considerable power to dictate prices, has left about 500,000 customers scrambling to find health insurance for next year. A ninth co-op, which served Iowa and Nebraska, closed in February.

At a time when the industry is experiencing a wave of consolidation, with giants like Anthem and Aetna planning to buy their smaller rivals, the vanishing co-ops will leave some consumers with fewer choices — and potentially higher prices.

The failures include co-ops in New York, Colorado, Kentucky and South Carolina.

The shuttering of these start-ups amounts to what could be a loss of nearly $1 billion in federal loans provided to help them get started. And the cascading series of failures has also led to skepticism about the Obama administration’s commitment to this venture.

UPDATE: A day after this was posted, another IRS co-op has just closed, this time in Utah. Now we are up to 10 out of 22.

Cato Institute health care expert Michael Tanner talks about the increases in health care premiums caused by Obamacare at CNS News:

For example, insurance companies have begun submitting their requests for rate increases for 2016, and those requests suggest that premiums could skyrocket next year. Already we’ve seen requests for increases for individual plans as high as 64.8 percent in Texas, 61 percent in Pennsylvania, 51.6 percent in New Mexico, 36.3 percent in Tennessee, 30.4 percent in Maryland, 25 percent in Oregon, and 19.9 percent in Washington. Those increases would come on top of premium increases last year that were 24.4 percent above what they would have been without Obamacare, according to a study from the National Bureau of Economic Research. At the same time, deductibles for the cheapest Obamacare plans now average about $5,180 for individuals and $10,500 for families.

Recall that on this blog, pretty much all of 2009 and 2010 was spent carefully explaining the moral hazards and other problems created by Obamacare. This was stuff that Republicans knew would happen. But on the other side of the aisle, there was too much naive, youthful exuberance from the secular left. Evidence was ignored, and feelings won the day. Obamacare was passed on the memes and tweets, while the studies reported by people like me went entirely unread.

Investors Business Daily just posted a list of 12 problems with Obamcare for the middle class:

Remember how many times I blogged about this one:

6. Shorter Workweeks

Because ObamaCare’s employer mandate fines don’t apply for workers who average fewer than 30 hours per week, the law gives companies an incentive to put a cap on workhours — particularly for low-wage workers who are less likely to be offered coverage.

The impact isn’t big enough to show up in economywide data, but there’s little doubt that the employer mandate has hurt a lot of people. IBD found 450 employers that capped workhours, and Current Population Survey data show a dive in the share of workers clocking just above 30 hours per week.

And what about the penalty for not buying what the government tells you to:

7. Impact On Wages

In 2016, a company with 50 full-time-equivalent workers could face a penalty of $2,160 per employee (with 30 workers exempted). When the after-tax fine is converted to tax-deductible wages, it equates to $1.71 an hour for a full-time worker.

Who will pay the penalty? For the most part, it won’t be employers — at least not directly. The CBO expects that “the penalty will be borne primarily by workers in the form of reduced wages or other compensation.”

Again, I want to emphasize that it is the evidence-hating secular left that is surprised by these “unexpected” problems with their childish policy. Those of us on the religious right predicted them, because we read the studies that were done before the 2012 election.

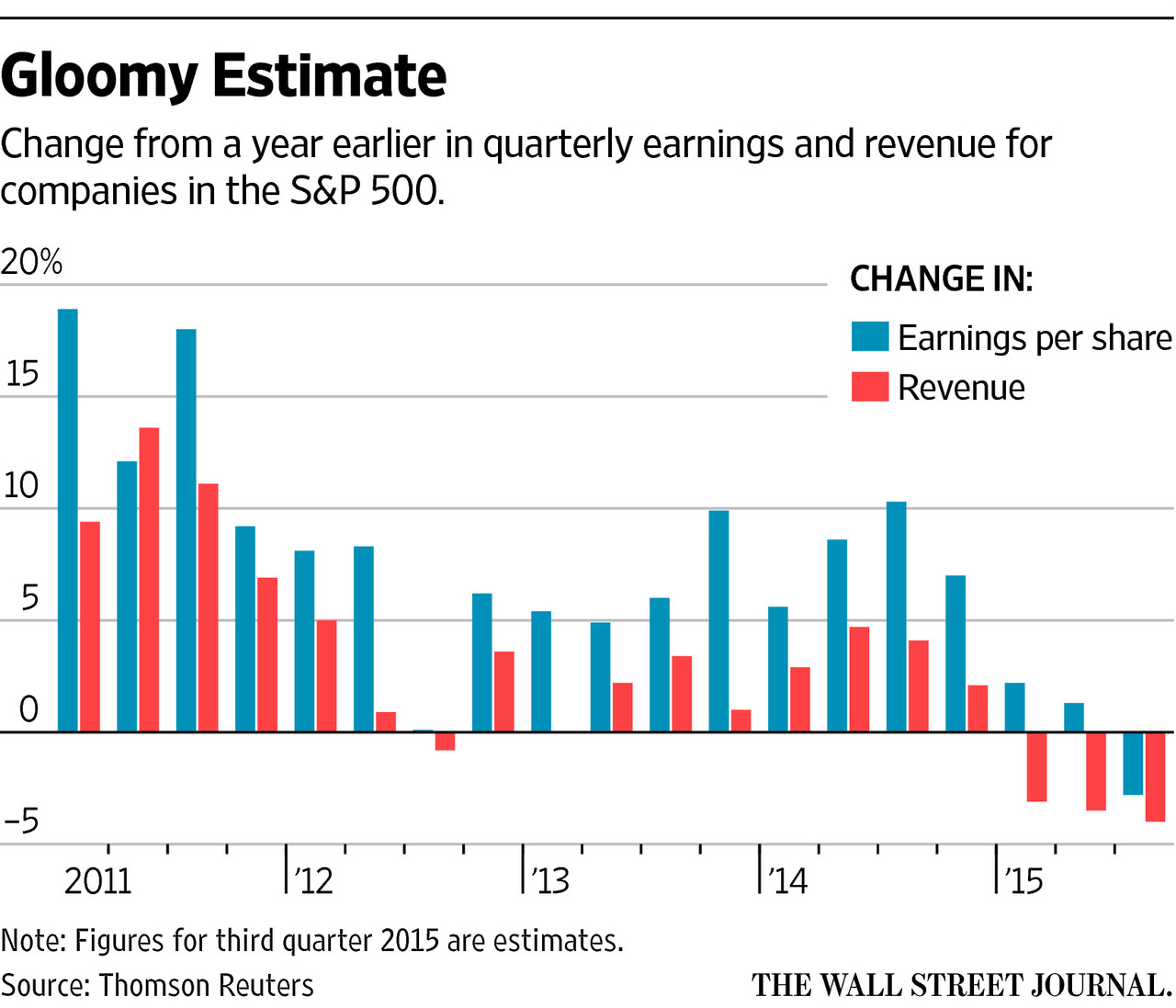

The Wall Street Journal reports that the economy’s not doing so well, either:

In 2006, we handed both the House and Senate to Democrats. The national debt was $8.5 trillion. In 2008, we handed the Presidency to the Democrats. The national debt was $10 trillion. After 10 years of Democrats, we now have a national debt of $18.5 trillion. It has been a long, low-interest, no-growth Keynesian binge. The kind of economics you expect from a socialist community organizer.

Even the “70% of the original projection” is deceptive. The measurement term they use is “uninsured”. The suggestion is that they are solving the problem of being “uninsured”. I’ve talked to people who have gone from “uninsured” to “insured” without any discernible benefit. They’ve told me about medical problems they’ve had. “But … you’re insured now. Why don’t you go to the doctor?” “Oh,” they tell me almost universally, “we can’t afford that.” Between the mandated cost and the large minimum deductibles, they are technically “insured”, but in practice can’t use that insurance any more than when they were uninsured. One told me, “It actually costs me more now to go to the emergency room because I have insurance with a huge deductible than it did when I had none.” I note that not too many are asking about this in the question of mandated healthcare reform.

LikeLike

There are lots of ways to lower the costs of health care with free-market reforms that take us towards a consumer-driven health care system. But we didn’t vote for Regina Hertzlinger, John C. Goodman, David Gratzer, Michael Tanner, Michael Cannon. Avik Roy, or Sally Pipes. We voted for the secular left imbecile. In fact, the names of recognized policy experts I just listed there are completely unknown to Democrat voters, who occupy their minds with tweets, memes and celebrity gossip. We can’t run a country when half the population is too stupid to vote.

LikeLike

I find that democracy with no minimum standard for intelligence in decision making has a number of problems. Policy is decided by popularity instead of reasoned based on facts.

LikeLike

If we had some sort of basic pre-vote test like “What is the name of your governor?” or “what are the names of your two senators?” or “what is the national debt to the nearest trillion?” then no one on the secular left would be qualified to vote. They can tweet memes to each other on Twitter and watch Stephen Colbert and Rachel Maddow, but they wouldn’t be able to affect what goes on in the real world of dollars and cents.

LikeLike

A test won’t do. Simple mandate that you have paid net taxes for 5 years before you get to vote.

LikeLike

Works for me. File tax returns 5 consecutive years.

LikeLike