Student loans became a huge problem when the Obama administration decided to take the decision about whether to grant the loans away from private sector loan managers and put it into the hands of politicians. Nationalizing student loans allowed Democrats to buy the votes of college students who wanted to get funding for degrees in Why Your Religious Parents Are Evil, which actually turn out to be Four Years of Drunken Hook-Up Sex. The trouble with this vote-buying plan was always how to deal with the loans after the four years are up. Well, how about continuing to buy the votes by passing the cost of the non-STEM degrees onto taxpayers? After all, working families don’t need the money, and it’s much better spent on beer and contraceptives, right? Responsible people don’t vote for Democrats anyway, so let’s just take their money and buy the votes of drunk promiscuous college students.

Here’s the story from the Wall Street Journal.

Excerpt:

Virginia Murphy borrowed a small fortune to attend law school and pursue her dream of becoming a public defender. Now the Florida resident is among an expanding breed of American borrower: those who owe at least $100,000 in student debt but have no expectation of paying it back.

Ms. Murphy pays just $330 a month—less than the interest on her $256,000 balance—under a federal income-based repayment program that has become one of the nation’s fastest-growing entitlements. She plans to use another federal program to have her balance forgiven in about seven years, a sum set to swell by then to $300,000.

The promise of forgiveness is “the only reason I would have ever considered” amassing so much debt to attend Tulane University Law School, says Ms. Murphy, 45 years old. She earns $56,500 a year as an assistant public defender in West Palm Beach.

The doubling of student debt since the recession, to $1.19 trillion, has stoked a national discussion over how to rein in college costs and debt and is becoming a major issue in the 2016 presidential race.

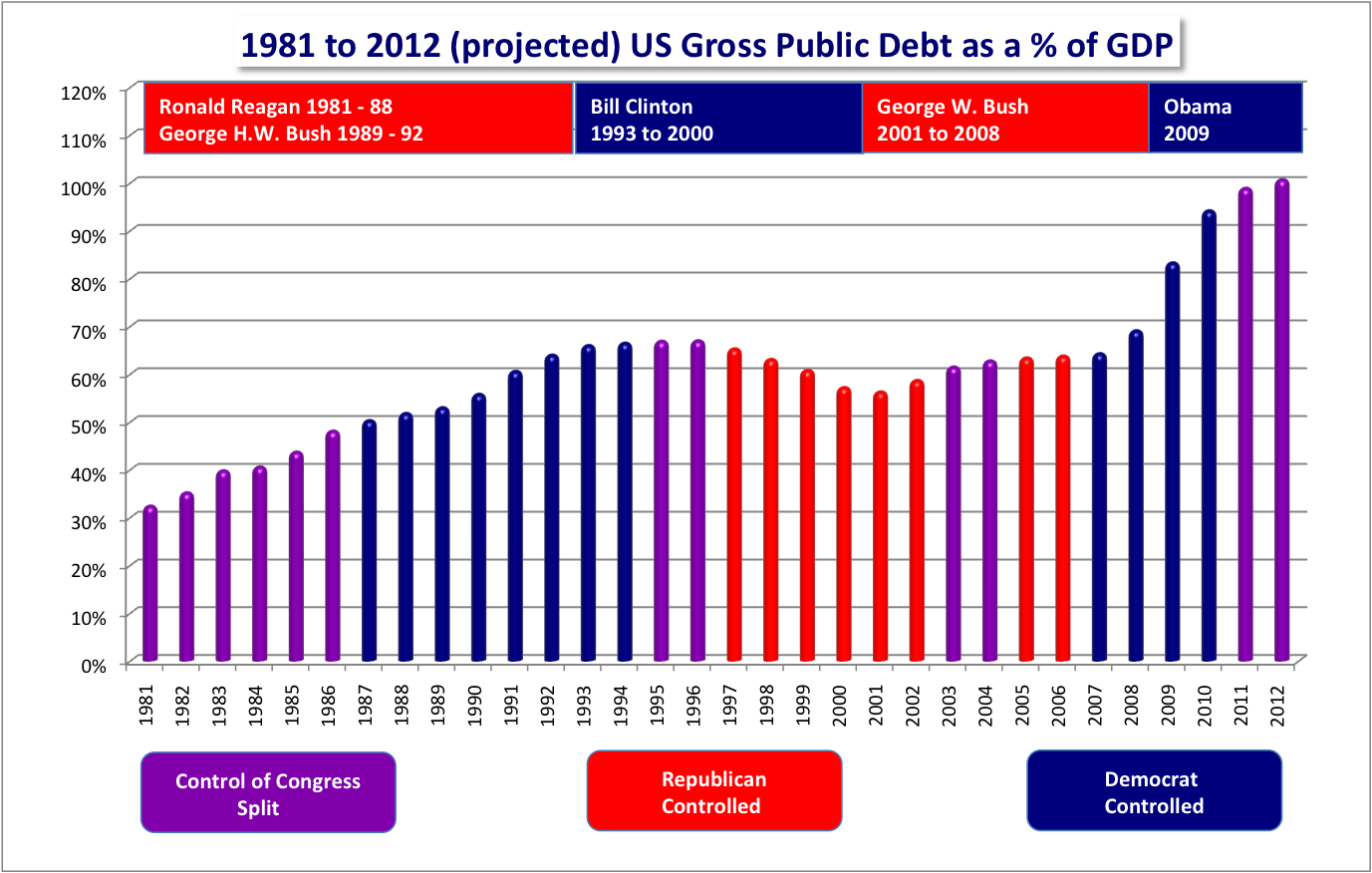

$300,000? That’s no problem. it was so good that we got Nancy Pelosi and Harry Reid to spend more money in 2007:

(Click for larger image)

More:

Federal programs allow grad students to borrow essentially unlimited amounts—whatever their schools charge—while requiring only a scant credit check and no assessment of their ability to repay. Other government loan programs, such as those for undergraduate students and home buyers, set loan limits to prevent borrowers from getting too deep into debt. Undergraduates are capped at $57,500 total in federal loans.

As graduate-school enrollment swelled over the past decade, the number of Americans owing at least $100,000 in student debt more than quintupled to 1.82 million as of Jan. 1, New York Federal Reserve data show. The number of all student borrowers nearly doubled to 43.34 million.

[…]The federal student-loan programs are designed to generate revenue for taxpayers, and they do. But surging enrollment in the debt-forgiveness programs recently prompted the government to increase by $22 billion its estimate of the long-term costs of the provisions. And a recent move to expand the most generous repayment program to millions more borrowers will cost an estimated $15.3 billion.

Critics say offering unlimited loans to students, with the prospect of forgiveness, creates a moral hazard by allowing borrowers to amass debts they have little hope or intention of repaying, all while enriching institutions and leaving taxpayers to pick up the tab.

Moral hazard? What’s that? Maybe Hillary Clinton knows.

She has announced an interesting plan about how to deal with people doing useless degrees that are really just a lot of drinking, partying and promiscuity. More spending to buy more votes – transfer well from responsible working families to drunken promiscuous students studying non-STEM degrees, because STEM degrees that will actually get them jobs are too hard.

Excerpt:

The hard truth on the student-loan crisis is that the problem is not being caused by a lack of money. It’s quite the opposite. A recent study by the New York Federal Reserve validated the long-held concerns of many economists and policy analysts alike when it found that “on average, for a $1 increase in the subsidized-loan cap, tuitions rose by as much as 65 cents.” In short, there is too much money available for the taking by colleges and universities because of generous government loans. This is driving up tuition prices. If the government just keeps increasing how much it is willing to lend students, where is the incentive for schools to control costs? Universities are currently engaged in an amenities arms race to attract students and their loan dollars. One need not look any further for evidence of this than ESPN on a Saturday afternoon in the fall or a student-life brochure. Texas Tech University has a waterpark on campus for goodness’ sake, and LSU is racing to finish one as well. How is $350 billion more dollars for universities to waste a solution of any sort? Mrs. Clinton’s preferred channels for delivering these funds are problematic as well. First, the plan calls for a cut in loan interest rates. Is this seriously something we’re willing to let politicians continue to get away with? Did we learn nothing from the housing crisis? Interest rates aren’t arbitrary figures without purpose — they are supposed to measure the risk of the borrower’s not being able to repay the lender. Judging by the severity of the present student-loan crisis and the number of defaulters, it’s safe to say interest rates are already too low. Additionally, interest rates are the price of borrowing money. Let’s think back to Economics 101 and remember what happens to demand when prices go down. How do we solve the crisis of rampant student loan debt by making it easier and more attractive to get into? It doesn’t matter if the interest rate on $150,000 is zero percent when you still owe $150,000 and you’re unemployed. Students don’t need a lower interest rate. They need colleges to constrain spending. Further, they need high-paying jobs. Of course, the Clinton plan only makes the latter problem worse as well. Under the Hillary’s plan, states will be encouraged to offer “no loan” tuition at four-year universities and free two-year community college through the promise of federal tax dollars. Of course, those tax dollars will have to come from somewhere. This is yet another drain on private business whose resources could otherwise be creating jobs for existing unemployed and underemployed students and graduates. Some will say this part of the plan helps students, but on net the economic drag remains the same, with the burden of education inflation simply shifted from students to their potential employers.

She is obviously well-versed in how economics works, and not just some talentless clown who married a hot male slut and then turned a blind eye to his philandering so that she could get affirmative action appointments on her way to an affirmative action presidency. Most sexually-transmitted diseases don’t affect your judgment at all. So stop worrying, America. Everything is going to be fine.

Why is it that whenever we have elections, people on the left have nothing more to offer us than schemes to buy votes by shifting money from winners to losers? They have no idea how to grow the economy, create jobs, promote marriage and families, and disincentivize irresponsible, reckless behaviors. It’s all about borrowing from people in the womb, to pay for free stuff for losers, in order to get their votes. This inter-generational theft is evil. It is enslaving the unborn to serve the whims of new masters. Slavery is wrong.

I had a Federal Loan that I signed for in 1993. It was for graduate school. I borrowed for the two-year program over $73,000.00. I started payments in August 1995.

The interest was 8% at that time. Today’s low interest loans? i would have killed for a 3% or 2 1/2 % loan!

I PAID MY LOAN BACK. ALL OF IT.

It was hard. I had to sacrifice “fun” at times in my working career to pay a loan back. I still had to pay when I lost my job, and had to take one that “didn’t pay as much” as my previous one. When a payment was “late” (and a few were). That phone would RING! I was told by angry government workers that: “I knew what I was getting into” and that I had to “send the payment”

It took 24 years, but the bill was “closed” and “paid in full” in the summer of 2014. I have zero sympathy for these students.

Pay up!

LikeLike

24 years? My bad math kind readers. It was NINETEEN years. Apologies!

LikeLike